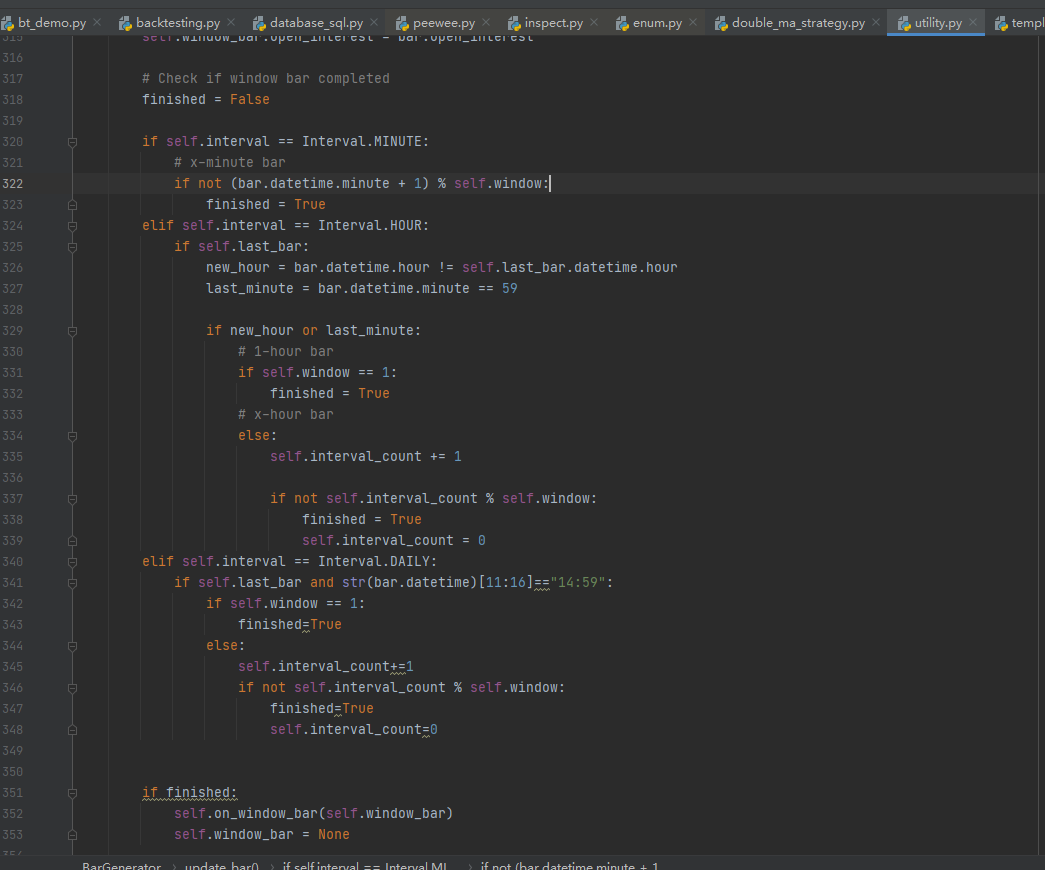

我的BarGenerator是这样的

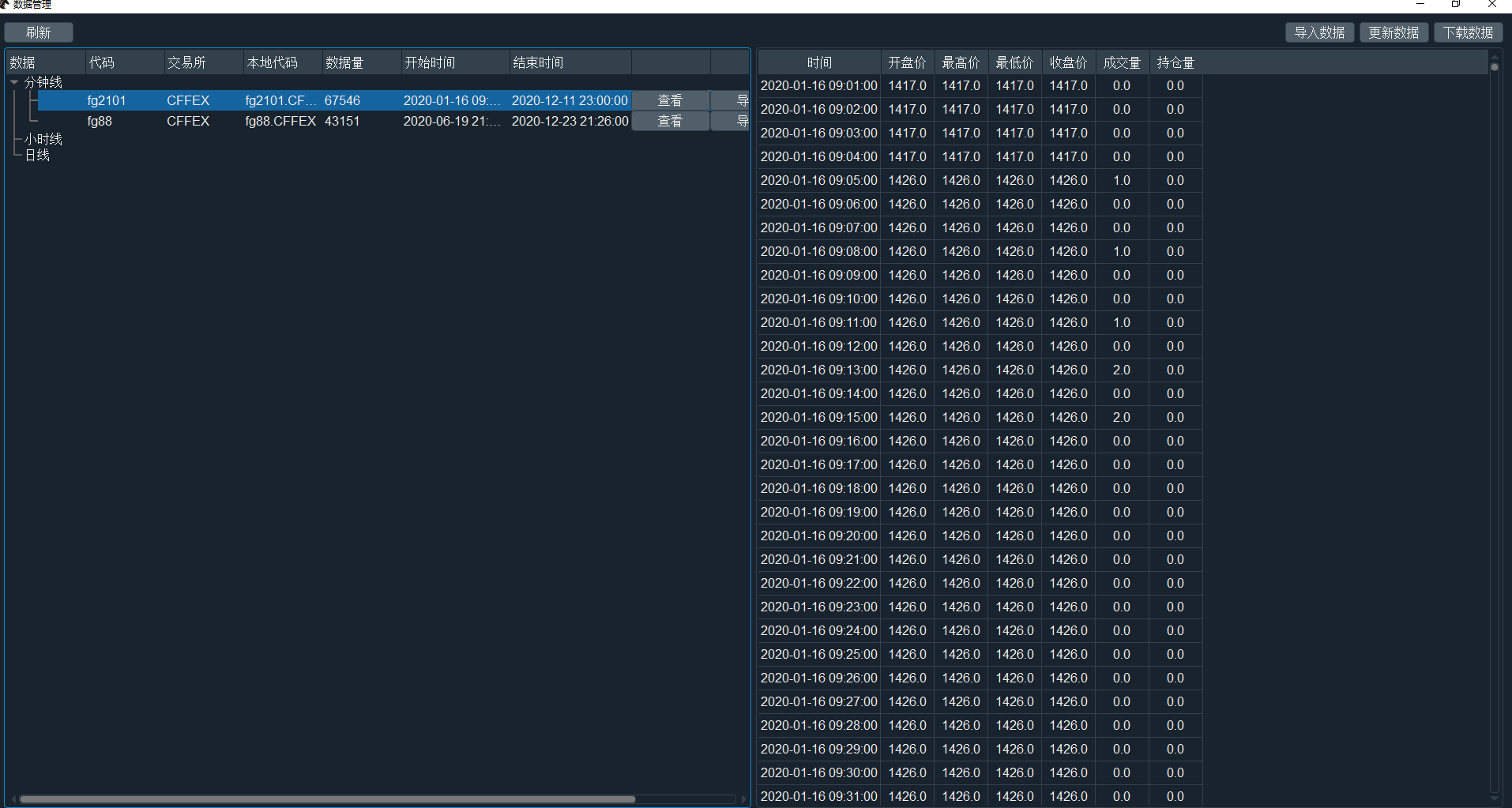

数据的日期是从20年1月16号开始的

结果输出的时候只有20年6月16号的数据,加载了少了半年才能合成第一根Bar

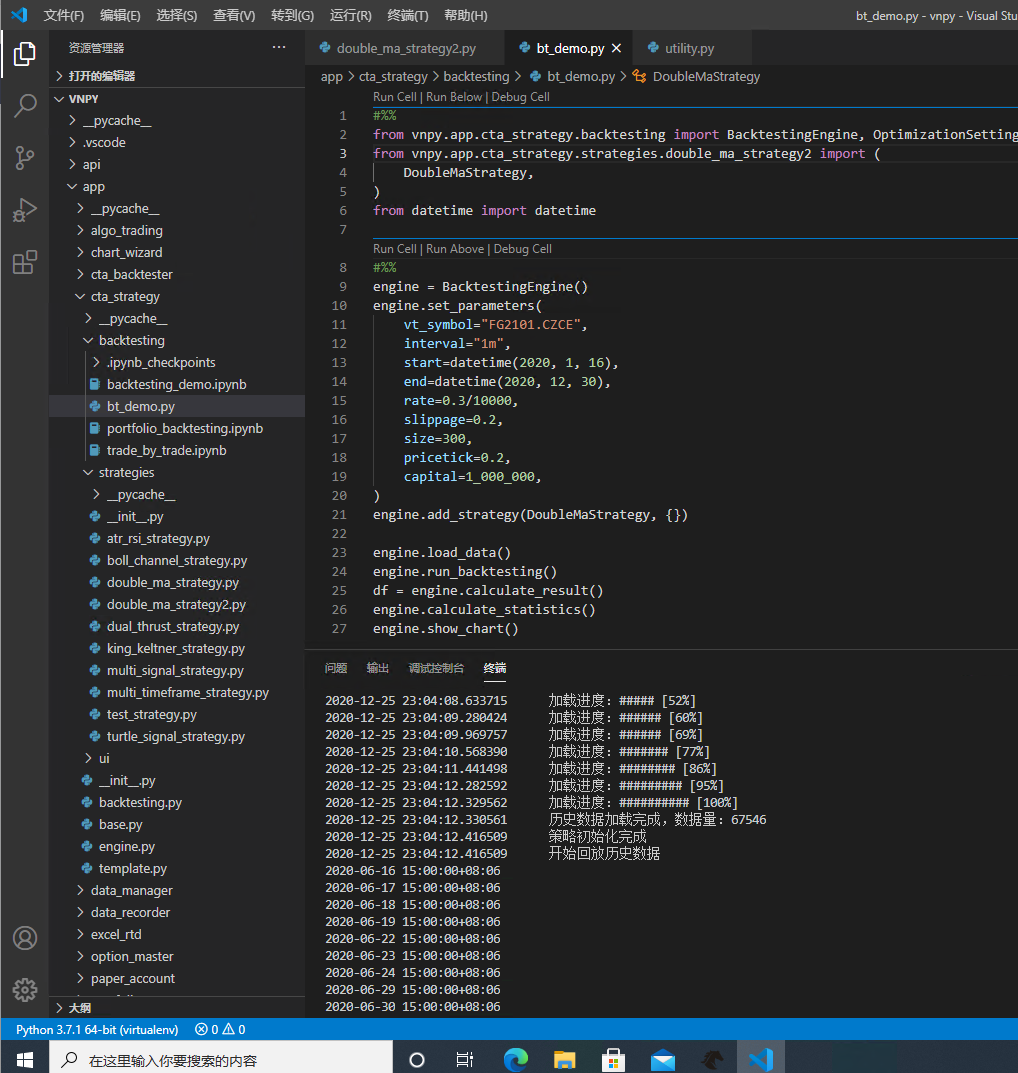

我换了好几台电脑都是这样,卸了重装还是一样 每次都是在BarGenerator下面加载了这段合成日线的代码

我以为我的原始数据有问题,但是我把Interval类型改为1分钟,1月16号的数据都可以每根都输出来

实在没办法了,下面是代码,大哥们帮我看下,谢谢!

from vnpy.app.cta_strategy import (

CtaTemplate,

StopOrder,

TickData,

BarData,

TradeData,

OrderData,

BarGenerator,

ArrayManager,

)

from vnpy.trader.constant import Interval

class DoubleMaStrategy(CtaTemplate):

author = "用Python的交易员"

fast_window = 10

slow_window = 20

fast_ma0 = 0.0

fast_ma1 = 0.0

slow_ma0 = 0.0

slow_ma1 = 0.0

parameters = ["fast_window", "slow_window"]

variables = ["fast_ma0", "fast_ma1", "slow_ma0", "slow_ma1"]

def __init__(self, cta_engine, strategy_name, vt_symbol, setting):

""""""

super().__init__(cta_engine, strategy_name, vt_symbol, setting)

self.bg = BarGenerator(self.on_bar)

self.am = ArrayManager()

self.bg_x=BarGenerator(self.on_bar,1,self.on_x_bar,interval=Interval.DAILY)

self.am_x = ArrayManager()

def on_init(self):

"""

Callback when strategy is inited.

"""

self.write_log("策略初始化")

self.load_bar(40)

def on_start(self):

"""

Callback when strategy is started.

"""

self.write_log("策略启动")

self.put_event()

def on_stop(self):

"""

Callback when strategy is stopped.

"""

self.write_log("策略停止")

self.put_event()

def on_tick(self, tick: TickData):

"""

Callback of new tick data update.

"""

self.bg.update_tick(tick)

def on_bar(self, bar: BarData):

"""

Callback of new bar data update.

"""

am = self.am

am.update_bar(bar)

self.bg_x.update_bar(bar)

if not am.inited:

return

pass

def on_x_bar(self,bar):

am = self.am_x

am.update_bar(bar)

if not am.inited:

return

pass

self.put_event()

print("on_day",bar.datetime)

def on_order(self, order: OrderData):

"""

Callback of new order data update.

"""

pass

def on_trade(self, trade: TradeData):

"""

Callback of new trade data update.

"""

self.put_event()

def on_stop_order(self, stop_order: StopOrder):

"""

Callback of stop order update.

"""

pass