from vnpy.app.cta_strategy import (

CtaTemplate,

BarGenerator,

ArrayManager,

Direction

)

from vnpy.trader.object import (

BarData,

TickData,

TradeData,

OrderData,

)

from typing import Any

from vnpy.trader.constant import Interval

from datetime import time

import datetime

class NewAtrStrategy(CtaTemplate):

""""""

author = ""

atr_window = 30

atr_cs = 6

zs = 20

fix_size = 1

bars = []

up_line = 0.0

down_line = 0.0

mid_line = 0.0

atr_value = 0.0

short_entry = 0.0

long_entry = 0.0

long_stop = 0.0

short_stop = 0.0

parameters = [

'atr_window',

'atr_cs',

'zs',

'fix_size'

]

variables = [

'up_line',

'down_line',

'atr_value'

]

def __init__(

self,

cta_engine: Any,

strategy_name: str,

vt_symbol: str,

setting: dict,

):

super().__init__(cta_engine,strategy_name,vt_symbol,setting)

self.bg5 = BarGenerator(self.on_bar,

window=5,

on_window_bar=self.on_5minutes_bar,

interval=Interval.MINUTE)

self.am5 = ArrayManager()

self.bars = []

def on_init(self):

"""策略引擎初始化"""

self.write_log("策略初始化")

self.load_bar(20)

def on_start(self):

"""策略启动"""

self.write_log("策略启动")

self.put_event()

def on_stop(self):

"""策略停止"""

self.write_log("策略停止")

self.put_event()

def on_tick(self,tick: TickData):

self.bg5.update_tick(tick)

def on_bar(self,bar:BarData):

self.bg5.update_bar(bar)

def on_5minutes_bar(self,bar:BarData):

self.cancel_all

am5 = self.am5

am5.update_bar(bar)

self.bars.append(bar)

if len(self.bars) <= 2:

return

else:

self.bars.pop(0)

last_bar = self.bars[-2]

if not am5.inited:

return

if last_bar.datetime.date() != bar.datetime.date():

self.mid_line = last_bar.close_price

art_array = am5.atr(self.atr_window, array=True)

self.atr_value = art_array[-1]

self.up_line = self.mid_line + self.atr_cs * self.atr_value

self.down_line = self.mid_line - self.atr_cs * self.atr_value

if self.pos == 0:

self.long_entry = 0

self.long_stop = 0

self.short_entry = 0

self.short_stop = 0

#上穿up_line做多

if bar.close_price >= self.up_line and last_bar.close_price < self.up_line:

price = bar.close_price

self.buy(price, self.fix_size)

#下穿down_line做空

elif bar.close_price <= self.down_line and last_bar.close_price > self.down_line:

price = bar.close_price

self.short(price, self.fix_size)

elif self.pos > 0:

#固定止损,用停止单

if self.long_stop:

self.sell(self.long_stop,self.pos,stop=True)

if bar.close_price <= self.down_line:

self.sell(bar.close_price,abs(self.pos),stop=True)

elif self.pos < 0:

#固定止损

if self.short_stop:

self.cover(self.short_stop,abs(self.pos),stop=True)

if bar.close_price >= self.up_line:

self.cover(bar.close_price,abs(self.pos),stop=True)

self.put_event()

def on_trade(self,trade: TradeData):

if self.pos != 0:

if trade.direction == Direction.LONG:

self.long_entry = trade.price

self.long_stop = self.long_entry * (1000-self.zs)/1000

else:

self.short_entry = trade.price

self.short_stop = self.short_entry * (1000 + self.zs)/1000

self.put_event()

def on_order(self,order: OrderData):

pass

def on_stop_order(self,order: OrderData):

pass

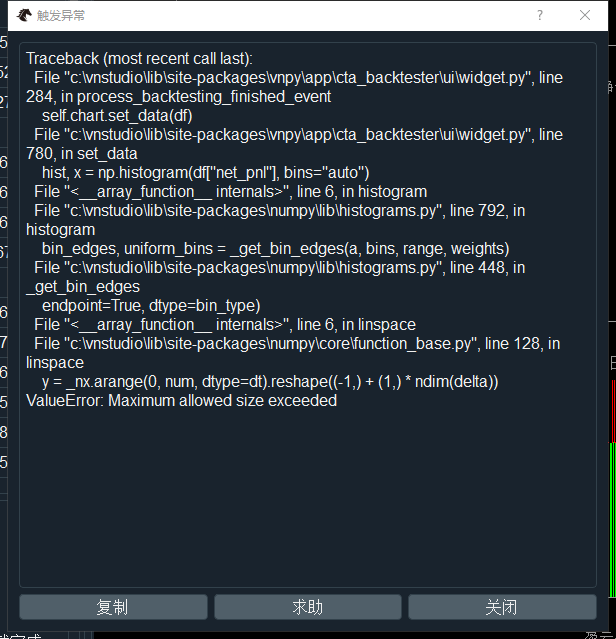

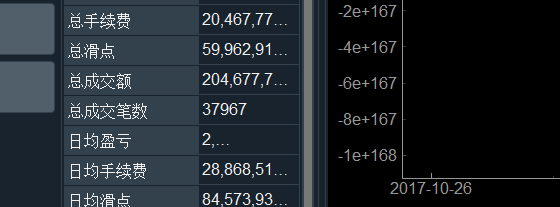

回测的问题是:

一:会报错

二:交易量巨大

求帮助啊,谢谢!