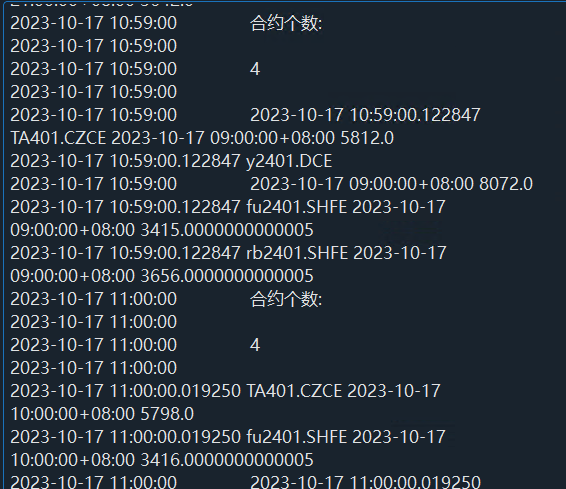

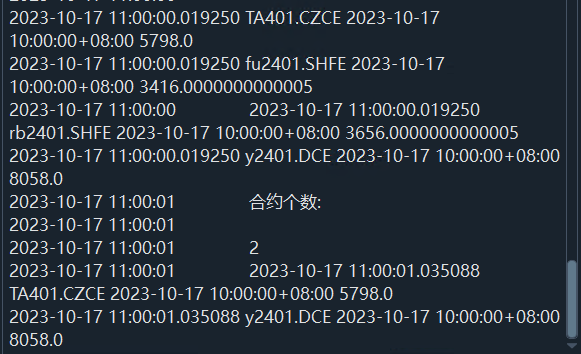

实盘,版本3.8,用PortfolioBollChannelStrategy测试,一个时间点推送了3次

from typing import List, Dict

from datetime import datetime

from vnpy.trader.utility import ArrayManager, Interval

from vnpy.trader.object import TickData, BarData

from vnpy_portfoliostrategy import StrategyTemplate, StrategyEngine

from vnpy_portfoliostrategy.utility import PortfolioBarGenerator

class PortfolioBollChannel1Strategy(StrategyTemplate):

"""组合布林带通道策略"""

author = "用Python的交易员"

boll_window = 18

boll_dev = 3.4

cci_window = 10

atr_window = 30

sl_multiplier = 5.2

fixed_size = 1

price_add = 5

parameters = [

"boll_window",

"boll_dev",

"cci_window",

"atr_window",

"sl_multiplier",

"fixed_size",

"price_add"

]

variables = []

def __init__(

self,

strategy_engine: StrategyEngine,

strategy_name: str,

vt_symbols: List[str],

setting: dict

) -> None:

"""构造函数"""

super().__init__(strategy_engine, strategy_name, vt_symbols, setting)

self.boll_up: Dict[str, float] = {}

self.boll_down: Dict[str, float] = {}

self.cci_value: Dict[str, float] = {}

self.atr_value: Dict[str, float] = {}

self.intra_trade_high: Dict[str, float] = {}

self.intra_trade_low: Dict[str, float] = {}

self.targets: Dict[str, int] = {}

self.last_tick_time: datetime = None

# 获取合约信息

self.ams: Dict[str, ArrayManager] = {}

for vt_symbol in self.vt_symbols:

self.ams[vt_symbol] = ArrayManager()

self.targets[vt_symbol] = 0

self.pbg = PortfolioBarGenerator(

self.on_bars, 2, self.on_2hour_bars, Interval.HOUR)

def on_init(self) -> None:

"""策略初始化回调"""

self.write_log("策略初始化")

self.load_bars(15)

def on_start(self) -> None:

"""策略启动回调"""

self.write_log("策略启动")

def on_stop(self) -> None:

"""策略停止回调"""

self.write_log("策略停止")

def on_tick(self, tick: TickData) -> None:

"""行情推送回调"""

self.pbg.update_tick(tick)

def on_bars(self, bars: Dict[str, BarData]) -> None:

"""K线切片回调"""

self.pbg.update_bars(bars)

def on_2hour_bars(self, bars: Dict[str, BarData]) -> None:

"""2小时K线回调"""

self.cancel_all()

print("合约个数:", len(bars))

# 更新到缓存序列

for vt_symbol, bar in bars.items():

am: ArrayManager = self.ams[vt_symbol]

am.update_bar(bar)

for vt_symbol, bar in bars.items():

am: ArrayManager = self.ams[vt_symbol]

if not am.inited:

return

print(datetime.now(), vt_symbol, bar.datetime, bar.close_price)

# 推送界面更新

self.put_event()