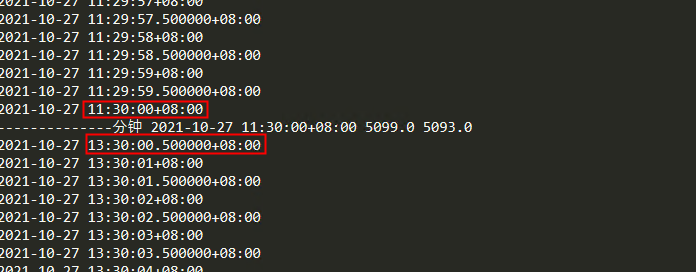

BarGenerator通过tick时时行情在合成数据时发现一个问题,如下图:

就是在跨交易时间段,比如上午11:30跟下午13:30衔接时段会出现上午11:30的k到下午才推出来,但是仔细看这跟k,其实只有1根tick数据,而上午11:59:59.500000时间推送出去的11:59的bar其实就差1根tick,深究代码:

def update_tick(self, tick: TickData) -> None:

"""

Update new tick data into generator.

"""

new_minute = False

# Filter tick data with 0 last price

if not tick.last_price:

return

# Filter tick data with older timestamp

if self.last_tick and tick.datetime < self.last_tick.datetime:

return

if not self.bar:

new_minute = True

elif (

(self.bar.datetime.minute != tick.datetime.minute)

or (self.bar.datetime.hour != tick.datetime.hour)

):

self.bar.datetime = self.bar.datetime.replace(

second=0, microsecond=0

)

self.on_bar(self.bar)

new_minute = True

if new_minute:

self.bar = BarData(

symbol=tick.symbol,

exchange=tick.exchange,

interval=Interval.MINUTE,

datetime=tick.datetime,

gateway_name=tick.gateway_name,

open_price=tick.last_price,

high_price=tick.last_price,

low_price=tick.last_price,

close_price=tick.last_price,

open_interest=tick.open_interest

)

else:

self.bar.high_price = max(self.bar.high_price, tick.last_price)

if tick.high_price > self.last_tick.high_price:

self.bar.high_price = max(self.bar.high_price, tick.high_price)

self.bar.low_price = min(self.bar.low_price, tick.last_price)

if tick.low_price < self.last_tick.low_price:

self.bar.low_price = min(self.bar.low_price, tick.low_price)

self.bar.close_price = tick.last_price

self.bar.open_interest = tick.open_interest

self.bar.datetime = tick.datetime

if self.last_tick:

volume_change = tick.volume - self.last_tick.volume

self.bar.volume += max(volume_change, 0)

turnover_change = tick.turnover - self.last_tick.turnover

self.bar.turnover += max(turnover_change, 0)

self.last_tick = tick发现在运行 self.on_bar(self.bar) 时并没有把从59秒变成00秒的那根tick数据加进去,实际只推送出去59.500000秒的数据,在常规时段因为不会出现如11:30:00至14:30:00这种秒级别的0跟0的衔接,所以数据不会有异常,当跨时段时就出现该问题,此时会导致衔接时段收到的如1分钟k线只有1根tick的数据,从而影响如均线的计算的准确性。

解决方案:

def update_tick(self, tick: TickData) -> None:

"""

Update new tick data into generator.

"""

# Filter tick data with 0 last price

if not tick.last_price:

return

# Filter tick data with older timestamp

if self.last_tick and tick.datetime < self.last_tick.datetime:

return

if self.bar:

self.bar.high_price = max(self.bar.high_price, tick.last_price)

if tick.high_price > self.last_tick.high_price:

self.bar.high_price = max(self.bar.high_price, tick.high_price)

self.bar.low_price = min(self.bar.low_price, tick.last_price)

if tick.low_price < self.last_tick.low_price:

self.bar.low_price = min(self.bar.low_price, tick.low_price)

self.bar.close_price = tick.last_price

self.bar.open_interest = tick.open_interest

self.bar.datetime = tick.datetime

else:

self.bar = BarData(

symbol=tick.symbol,

exchange=tick.exchange,

interval=Interval.MINUTE,

datetime=tick.datetime,

gateway_name=tick.gateway_name,

open_price=tick.last_price,

high_price=tick.last_price,

low_price=tick.last_price,

close_price=tick.last_price,

open_interest=tick.open_interest

)

if self.last_tick:

volume_change = tick.volume - self.last_tick.volume

self.bar.volume += max(volume_change, 0)

turnover_change = tick.turnover - self.last_tick.turnover

self.bar.turnover += max(turnover_change, 0)

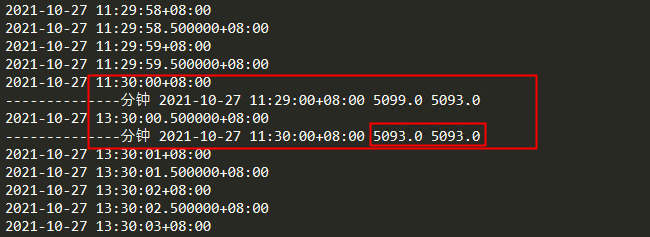

if self.last_tick and not (tick.datetime.replace(microsecond=0).second == 0 and self.last_tick.datetime.replace(microsecond=0).second == 0):

if self.last_tick and (

(self.last_tick.datetime.minute != tick.datetime.minute)

or (self.last_tick.datetime.hour != tick.datetime.hour)

):

self.bar.datetime = self.bar.datetime.replace(

second=0, microsecond=0

)

self.on_bar(self.bar)

self.bar = None

self.last_tick = tick结果如下: