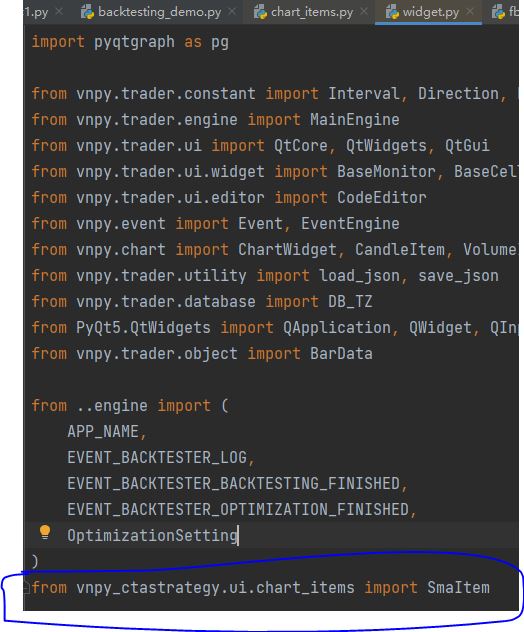

在原文件的基础上稍作修改,主要修改文件为vnpy\app\cta_backtester\ui\widget.py

import csv

from datetime import datetime, timedelta

from tzlocal import get_localzone

import numpy as np

import pyqtgraph as pg

from vnpy.trader.constant import Interval, Direction, Offset

from vnpy.trader.engine import MainEngine

from vnpy.trader.ui import QtCore, QtWidgets, QtGui

from vnpy.trader.ui.widget import BaseMonitor, BaseCell, DirectionCell, EnumCell

from vnpy.trader.ui.editor import CodeEditor

from vnpy.event import Event, EventEngine

from vnpy.chart import ChartWidget, CandleItem, VolumeItem

from vnpy.trader.utility import load_json, save_json

from vnpy.trader.constant import Exchange, Interval

from vnpy.trader.object import BarData

from PyQt5.QtWidgets import QApplication, QWidget, QInputDialog, QLineEdit

from ..engine import (

APP_NAME,

EVENT_BACKTESTER_LOG,

EVENT_BACKTESTER_BACKTESTING_FINISHED,

EVENT_BACKTESTER_OPTIMIZATION_FINISHED,

OptimizationSetting

)

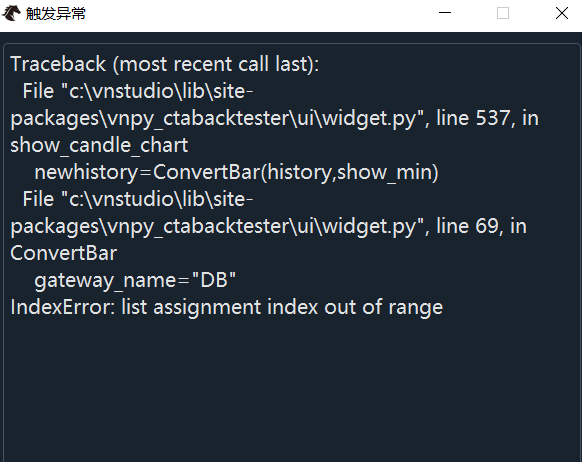

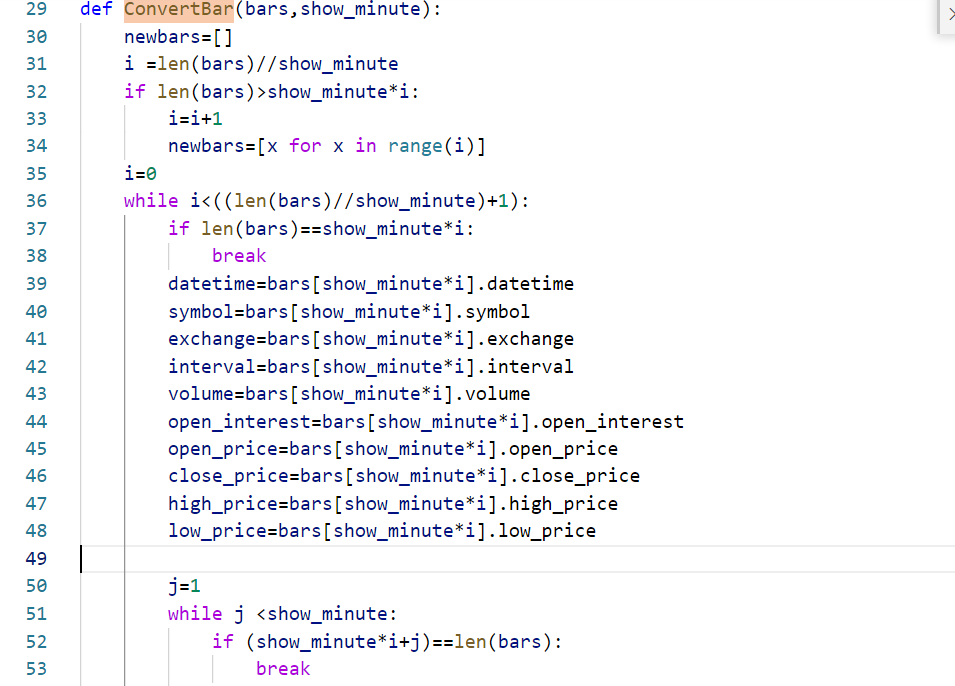

*def ConvertBar(bars,show_minute):

newbars=[]

i=len(bars)//show_minute

if len(bars)>show_minutei:

i=i+1

newbars=[x for x in range(i)]

i=0

while i<((len(bars)//show_minute)+1):

if len(bars)==show_minute*i:

break

datetime=bars[show_minute*i].datetime

symbol=bars[show_minute*i].symbol

exchange=bars[show_minute*i].exchange

interval=bars[show_minute*i].interval

volume=bars[show_minute*i].volume

open_interest=bars[show_minute*i].open_interest

open_price=bars[show_minute*i].open_price

close_price=bars[show_minute*i].close_price

high_price=bars[show_minute*i].high_price

low_price=bars[show_minute*i].low_price

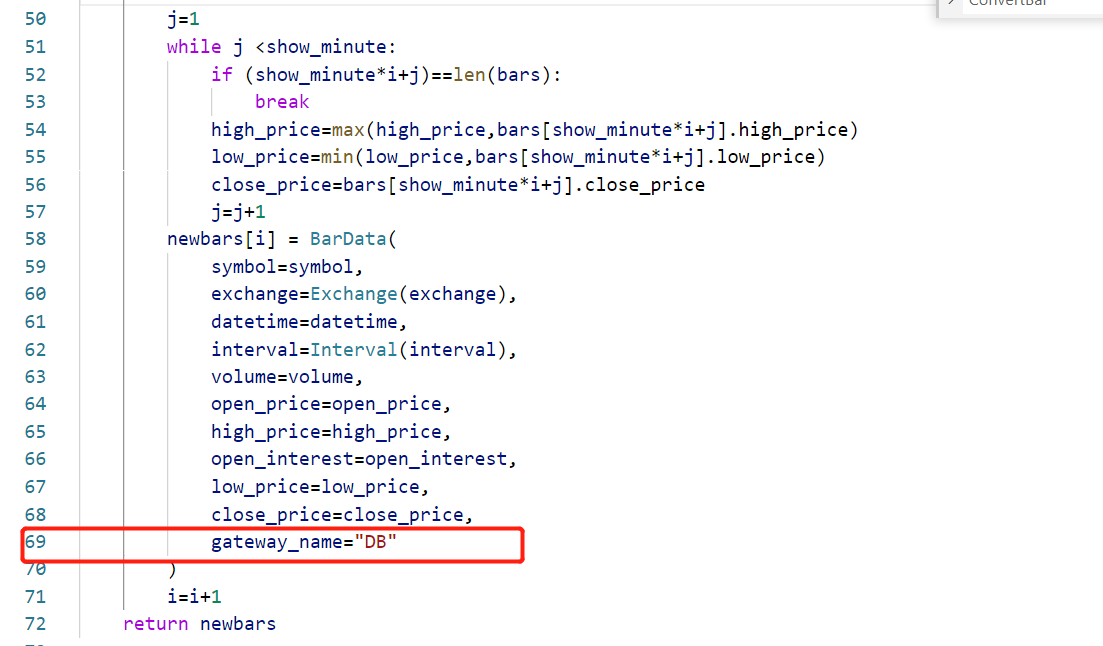

j=1

while j <show_minute:

if (show_minute*i+j)==len(bars):

break

high_price=max(high_price,bars[show_minute*i+j].high_price)

low_price=min(low_price,bars[show_minute*i+j].low_price)

close_price=bars[show_minute*i+j].close_price

j=j+1

newbars[i] = BarData(

symbol=symbol,

exchange=Exchange(exchange),

datetime=datetime,

interval=Interval(interval),

volume=volume,

open_price=open_price,

high_price=high_price,

open_interest=open_interest,

low_price=low_price,

close_price=close_price,

gateway_name="DB"

)

i=i+1

return newbars

**

class BacktesterManager(QtWidgets.QWidget):

""""""

setting_filename = "cta_backtester_setting.json"

signal_log = QtCore.pyqtSignal(Event)

signal_backtesting_finished = QtCore.pyqtSignal(Event)

signal_optimization_finished = QtCore.pyqtSignal(Event)

def __init__(self, main_engine: MainEngine, event_engine: EventEngine):

""""""

super().__init__()

self.main_engine = main_engine

self.event_engine = event_engine

self.backtester_engine = main_engine.get_engine(APP_NAME)

self.class_names = []

self.settings = {}

self.target_display = ""

self.init_ui()

self.register_event()

self.backtester_engine.init_engine()

self.init_strategy_settings()

self.load_backtesting_setting()

def init_strategy_settings(self):

""""""

self.class_names = self.backtester_engine.get_strategy_class_names()

for class_name in self.class_names:

setting = self.backtester_engine.get_default_setting(class_name)

self.settings[class_name] = setting

self.class_combo.addItems(self.class_names)

def init_ui(self):

""""""

self.setWindowTitle("CTA回测")

# Setting Part

self.class_combo = QtWidgets.QComboBox()

self.symbol_line = QtWidgets.QLineEdit("IF88.CFFEX")

self.interval_combo = QtWidgets.QComboBox()

for inteval in Interval:

self.interval_combo.addItem(inteval.value)

end_dt = datetime.now()

start_dt = end_dt - timedelta(days=3 * 365)

self.start_date_edit = QtWidgets.QDateEdit(

QtCore.QDate(

start_dt.year,

start_dt.month,

start_dt.day

)

)

self.end_date_edit = QtWidgets.QDateEdit(

QtCore.QDate.currentDate()

)

self.rate_line = QtWidgets.QLineEdit("0.000025")

self.slippage_line = QtWidgets.QLineEdit("0.2")

self.size_line = QtWidgets.QLineEdit("300")

self.pricetick_line = QtWidgets.QLineEdit("0.2")

self.capital_line = QtWidgets.QLineEdit("1000000")

self.inverse_combo = QtWidgets.QComboBox()

self.inverse_combo.addItems(["正向", "反向"])

backtesting_button = QtWidgets.QPushButton("开始回测")

backtesting_button.clicked.connect(self.start_backtesting)

optimization_button = QtWidgets.QPushButton("参数优化")

optimization_button.clicked.connect(self.start_optimization)

self.result_button = QtWidgets.QPushButton("优化结果")

self.result_button.clicked.connect(self.show_optimization_result)

self.result_button.setEnabled(False)

downloading_button = QtWidgets.QPushButton("下载数据")

downloading_button.clicked.connect(self.start_downloading)

self.order_button = QtWidgets.QPushButton("委托记录")

self.order_button.clicked.connect(self.show_backtesting_orders)

self.order_button.setEnabled(False)

self.trade_button = QtWidgets.QPushButton("成交记录")

self.trade_button.clicked.connect(self.show_backtesting_trades)

self.trade_button.setEnabled(False)

self.daily_button = QtWidgets.QPushButton("每日盈亏")

self.daily_button.clicked.connect(self.show_daily_results)

self.daily_button.setEnabled(False)

self.candle_button = QtWidgets.QPushButton("K线图表")

self.candle_button.clicked.connect(self.show_candle_chart)

self.candle_button.setEnabled(False)

edit_button = QtWidgets.QPushButton("代码编辑")

edit_button.clicked.connect(self.edit_strategy_code)

reload_button = QtWidgets.QPushButton("策略重载")

reload_button.clicked.connect(self.reload_strategy_class)

for button in [

backtesting_button,

optimization_button,

downloading_button,

self.result_button,

self.order_button,

self.trade_button,

self.daily_button,

self.candle_button,

edit_button,

reload_button

]:

button.setFixedHeight(button.sizeHint().height() * 2)

form = QtWidgets.QFormLayout()

form.addRow("交易策略", self.class_combo)

form.addRow("本地代码", self.symbol_line)

form.addRow("K线周期", self.interval_combo)

form.addRow("开始日期", self.start_date_edit)

form.addRow("结束日期", self.end_date_edit)

form.addRow("手续费率", self.rate_line)

form.addRow("交易滑点", self.slippage_line)

form.addRow("合约乘数", self.size_line)

form.addRow("价格跳动", self.pricetick_line)

form.addRow("回测资金", self.capital_line)

form.addRow("合约模式", self.inverse_combo)

result_grid = QtWidgets.QGridLayout()

result_grid.addWidget(self.trade_button, 0, 0)

result_grid.addWidget(self.order_button, 0, 1)

result_grid.addWidget(self.daily_button, 1, 0)

result_grid.addWidget(self.candle_button, 1, 1)

left_vbox = QtWidgets.QVBoxLayout()

left_vbox.addLayout(form)

left_vbox.addWidget(backtesting_button)

left_vbox.addWidget(downloading_button)

left_vbox.addStretch()

left_vbox.addLayout(result_grid)

left_vbox.addStretch()

left_vbox.addWidget(optimization_button)

left_vbox.addWidget(self.result_button)

left_vbox.addStretch()

left_vbox.addWidget(edit_button)

left_vbox.addWidget(reload_button)

# Result part

self.statistics_monitor = StatisticsMonitor()

self.log_monitor = QtWidgets.QTextEdit()

self.log_monitor.setMaximumHeight(400)

self.chart = BacktesterChart()

self.chart.setMinimumWidth(1000)

self.trade_dialog = BacktestingResultDialog(

self.main_engine,

self.event_engine,

"回测成交记录",

BacktestingTradeMonitor

)

self.order_dialog = BacktestingResultDialog(

self.main_engine,

self.event_engine,

"回测委托记录",

BacktestingOrderMonitor

)

self.daily_dialog = BacktestingResultDialog(

self.main_engine,

self.event_engine,

"回测每日盈亏",

DailyResultMonitor

)

# Candle Chart

self.candle_dialog = CandleChartDialog()

# Layout

vbox = QtWidgets.QVBoxLayout()

vbox.addWidget(self.statistics_monitor)

vbox.addWidget(self.log_monitor)

hbox = QtWidgets.QHBoxLayout()

hbox.addLayout(left_vbox)

hbox.addLayout(vbox)

hbox.addWidget(self.chart)

self.setLayout(hbox)

# Code Editor

self.editor = CodeEditor(self.main_engine, self.event_engine)

def load_backtesting_setting(self):

""""""

setting = load_json(self.setting_filename)

if not setting:

return

self.class_combo.setCurrentIndex(

self.class_combo.findText(setting["class_name"])

)

self.symbol_line.setText(setting["vt_symbol"])

self.interval_combo.setCurrentIndex(

self.interval_combo.findText(setting["interval"])

)

self.rate_line.setText(str(setting["rate"]))

self.slippage_line.setText(str(setting["slippage"]))

self.size_line.setText(str(setting["size"]))

self.pricetick_line.setText(str(setting["pricetick"]))

self.capital_line.setText(str(setting["capital"]))

if not setting["inverse"]:

self.inverse_combo.setCurrentIndex(0)

else:

self.inverse_combo.setCurrentIndex(1)

def register_event(self):

""""""

self.signal_log.connect(self.process_log_event)

self.signal_backtesting_finished.connect(

self.process_backtesting_finished_event)

self.signal_optimization_finished.connect(

self.process_optimization_finished_event)

self.event_engine.register(EVENT_BACKTESTER_LOG, self.signal_log.emit)

self.event_engine.register(

EVENT_BACKTESTER_BACKTESTING_FINISHED, self.signal_backtesting_finished.emit)

self.event_engine.register(

EVENT_BACKTESTER_OPTIMIZATION_FINISHED, self.signal_optimization_finished.emit)

def process_log_event(self, event: Event):

""""""

msg = event.data

self.write_log(msg)

def write_log(self, msg):

""""""

timestamp = datetime.now().strftime("%H:%M:%S")

msg = f"{timestamp}\t{msg}"

self.log_monitor.append(msg)

def process_backtesting_finished_event(self, event: Event):

""""""

statistics = self.backtester_engine.get_result_statistics()

self.statistics_monitor.set_data(statistics)

df = self.backtester_engine.get_result_df()

self.chart.set_data(df)

self.trade_button.setEnabled(True)

self.order_button.setEnabled(True)

self.daily_button.setEnabled(True)

self.candle_button.setEnabled(True)

def process_optimization_finished_event(self, event: Event):

""""""

self.write_log("请点击[优化结果]按钮查看")

self.result_button.setEnabled(True)

def start_backtesting(self):

""""""

class_name = self.class_combo.currentText()

vt_symbol = self.symbol_line.text()

interval = self.interval_combo.currentText()

start = self.start_date_edit.date().toPyDate()

end = self.end_date_edit.date().toPyDate()

rate = float(self.rate_line.text())

slippage = float(self.slippage_line.text())

size = float(self.size_line.text())

pricetick = float(self.pricetick_line.text())

capital = float(self.capital_line.text())

if self.inverse_combo.currentText() == "正向":

inverse = False

else:

inverse = True

# Save backtesting parameters

backtesting_setting = {

"class_name": class_name,

"vt_symbol": vt_symbol,

"interval": interval,

"rate": rate,

"slippage": slippage,

"size": size,

"pricetick": pricetick,

"capital": capital,

"inverse": inverse,

}

save_json(self.setting_filename, backtesting_setting)

# Get strategy setting

old_setting = self.settings[class_name]

dialog = BacktestingSettingEditor(class_name, old_setting)

i = dialog.exec()

if i != dialog.Accepted:

return

new_setting = dialog.get_setting()

self.settings[class_name] = new_setting

result = self.backtester_engine.start_backtesting(

class_name,

vt_symbol,

interval,

start,

end,

rate,

slippage,

size,

pricetick,

capital,

inverse,

new_setting

)

if result:

self.statistics_monitor.clear_data()

self.chart.clear_data()

self.trade_button.setEnabled(False)

self.order_button.setEnabled(False)

self.daily_button.setEnabled(False)

self.candle_button.setEnabled(False)

self.trade_dialog.clear_data()

self.order_dialog.clear_data()

self.daily_dialog.clear_data()

self.candle_dialog.clear_data()

def start_optimization(self):

""""""

class_name = self.class_combo.currentText()

vt_symbol = self.symbol_line.text()

interval = self.interval_combo.currentText()

start = self.start_date_edit.date().toPyDate()

end = self.end_date_edit.date().toPyDate()

rate = float(self.rate_line.text())

slippage = float(self.slippage_line.text())

size = float(self.size_line.text())

pricetick = float(self.pricetick_line.text())

capital = float(self.capital_line.text())

if self.inverse_combo.currentText() == "正向":

inverse = False

else:

inverse = True

parameters = self.settings[class_name]

dialog = OptimizationSettingEditor(class_name, parameters)

i = dialog.exec()

if i != dialog.Accepted:

return

optimization_setting, use_ga = dialog.get_setting()

self.target_display = dialog.target_display

self.backtester_engine.start_optimization(

class_name,

vt_symbol,

interval,

start,

end,

rate,

slippage,

size,

pricetick,

capital,

inverse,

optimization_setting,

use_ga

)

self.result_button.setEnabled(False)

def start_downloading(self):

""""""

vt_symbol = self.symbol_line.text()

interval = self.interval_combo.currentText()

start_date = self.start_date_edit.date()

end_date = self.end_date_edit.date()

start = datetime(

start_date.year(),

start_date.month(),

start_date.day(),

tzinfo=get_localzone()

)

end = datetime(

end_date.year(),

end_date.month(),

end_date.day(),

23,

59,

59,

tzinfo=get_localzone()

)

self.backtester_engine.start_downloading(

vt_symbol,

interval,

start,

end

)

def show_optimization_result(self):

""""""

result_values = self.backtester_engine.get_result_values()

dialog = OptimizationResultMonitor(

result_values,

self.target_display

)

dialog.exec_()

def show_backtesting_trades(self):

""""""

if not self.trade_dialog.is_updated():

trades = self.backtester_engine.get_all_trades()

self.trade_dialog.update_data(trades)

self.trade_dialog.exec_()

def show_backtesting_orders(self):

""""""

if not self.order_dialog.is_updated():

orders = self.backtester_engine.get_all_orders()

self.order_dialog.update_data(orders)

self.order_dialog.exec_()

def show_daily_results(self):

""""""

if not self.daily_dialog.is_updated():

results = self.backtester_engine.get_all_daily_results()

self.daily_dialog.update_data(results)

self.daily_dialog.exec_()

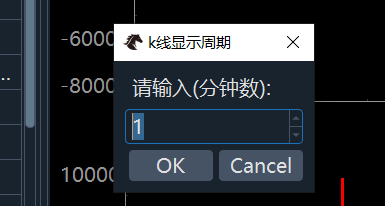

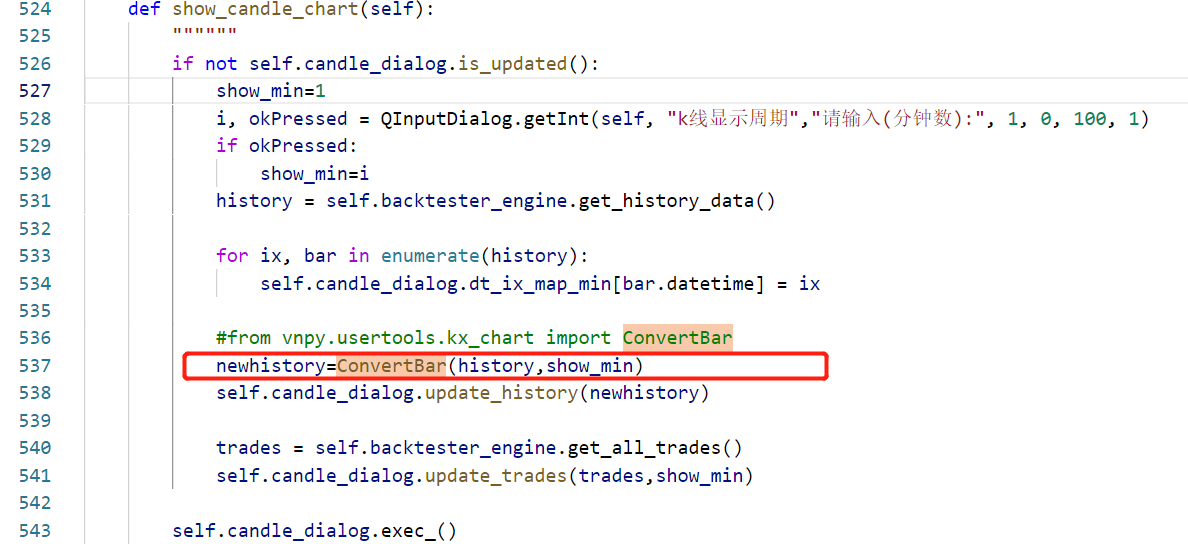

def show_candle_chart(self):

""""""

if not self.candle_dialog.is_updated():

show_min=1

i, okPressed = QInputDialog.getInt(self, "k线显示周期","请输入(分钟数):", 1, 0, 100, 1)

if okPressed:

show_min=i

history = self.backtester_engine.get_history_data()

for ix, bar in enumerate(history):

self.candle_dialog.dt_ix_map_min[bar.datetime] = ix

#from vnpy.usertools.kx_chart import ConvertBar

newhistory=ConvertBar(history,show_min)

self.candle_dialog.update_history(newhistory)

trades = self.backtester_engine.get_all_trades()

self.candle_dialog.update_trades(trades,show_min)

self.candle_dialog.exec_()

def edit_strategy_code(self):

""""""

class_name = self.class_combo.currentText()

file_path = self.backtester_engine.get_strategy_class_file(class_name)

self.editor.open_editor(file_path)

self.editor.show()

def reload_strategy_class(self):

""""""

self.backtester_engine.reload_strategy_class()

self.class_combo.clear()

self.init_strategy_settings()

def show(self):

""""""

self.showMaximized()

class StatisticsMonitor(QtWidgets.QTableWidget):

""""""

KEY_NAME_MAP = {

"start_date": "首个交易日",

"end_date": "最后交易日",

"total_days": "总交易日",

"profit_days": "盈利交易日",

"loss_days": "亏损交易日",

"capital": "起始资金",

"end_balance": "结束资金",

"total_return": "总收益率",

"annual_return": "年化收益",

"max_drawdown": "最大回撤",

"max_ddpercent": "百分比最大回撤",

"total_net_pnl": "总盈亏",

"total_commission": "总手续费",

"total_slippage": "总滑点",

"total_turnover": "总成交额",

"total_trade_count": "总成交笔数",

"daily_net_pnl": "日均盈亏",

"daily_commission": "日均手续费",

"daily_slippage": "日均滑点",

"daily_turnover": "日均成交额",

"daily_trade_count": "日均成交笔数",

"daily_return": "日均收益率",

"return_std": "收益标准差",

"sharpe_ratio": "夏普比率",

"return_drawdown_ratio": "收益回撤比"

}

def __init__(self):

""""""

super().__init__()

self.cells = {}

self.init_ui()

def init_ui(self):

""""""

self.setRowCount(len(self.KEY_NAME_MAP))

self.setVerticalHeaderLabels(list(self.KEY_NAME_MAP.values()))

self.setColumnCount(1)

self.horizontalHeader().setVisible(False)

self.horizontalHeader().setSectionResizeMode(

QtWidgets.QHeaderView.Stretch

)

self.setEditTriggers(self.NoEditTriggers)

for row, key in enumerate(self.KEY_NAME_MAP.keys()):

cell = QtWidgets.QTableWidgetItem()

self.setItem(row, 0, cell)

self.cells[key] = cell

def clear_data(self):

""""""

for cell in self.cells.values():

cell.setText("")

def set_data(self, data: dict):

""""""

data["capital"] = f"{data['capital']:,.2f}"

data["end_balance"] = f"{data['end_balance']:,.2f}"

data["total_return"] = f"{data['total_return']:,.2f}%"

data["annual_return"] = f"{data['annual_return']:,.2f}%"

data["max_drawdown"] = f"{data['max_drawdown']:,.2f}"

data["max_ddpercent"] = f"{data['max_ddpercent']:,.2f}%"

data["total_net_pnl"] = f"{data['total_net_pnl']:,.2f}"

data["total_commission"] = f"{data['total_commission']:,.2f}"

data["total_slippage"] = f"{data['total_slippage']:,.2f}"

data["total_turnover"] = f"{data['total_turnover']:,.2f}"

data["daily_net_pnl"] = f"{data['daily_net_pnl']:,.2f}"

data["daily_commission"] = f"{data['daily_commission']:,.2f}"

data["daily_slippage"] = f"{data['daily_slippage']:,.2f}"

data["daily_turnover"] = f"{data['daily_turnover']:,.2f}"

data["daily_return"] = f"{data['daily_return']:,.2f}%"

data["return_std"] = f"{data['return_std']:,.2f}%"

data["sharpe_ratio"] = f"{data['sharpe_ratio']:,.2f}"

data["return_drawdown_ratio"] = f"{data['return_drawdown_ratio']:,.2f}"

for key, cell in self.cells.items():

value = data.get(key, "")

cell.setText(str(value))

class BacktestingSettingEditor(QtWidgets.QDialog):

"""

For creating new strategy and editing strategy parameters.

"""

def __init__(

self, class_name: str, parameters: dict

):

""""""

super(BacktestingSettingEditor, self).__init__()

self.class_name = class_name

self.parameters = parameters

self.edits = {}

self.init_ui()

def init_ui(self):

""""""

form = QtWidgets.QFormLayout()

# Add vt_symbol and name edit if add new strategy

self.setWindowTitle(f"策略参数配置:{self.class_name}")

button_text = "确定"

parameters = self.parameters

for name, value in parameters.items():

type_ = type(value)

edit = QtWidgets.QLineEdit(str(value))

if type_ is int:

validator = QtGui.QIntValidator()

edit.setValidator(validator)

elif type_ is float:

validator = QtGui.QDoubleValidator()

edit.setValidator(validator)

form.addRow(f"{name} {type_}", edit)

self.edits[name] = (edit, type_)

button = QtWidgets.QPushButton(button_text)

button.clicked.connect(self.accept)

form.addRow(button)

widget = QtWidgets.QWidget()

widget.setLayout(form)

scroll = QtWidgets.QScrollArea()

scroll.setWidgetResizable(True)

scroll.setWidget(widget)

vbox = QtWidgets.QVBoxLayout()

vbox.addWidget(scroll)

self.setLayout(vbox)

def get_setting(self):

""""""

setting = {}

for name, tp in self.edits.items():

edit, type_ = tp

value_text = edit.text()

if type_ == bool:

if value_text == "True":

value = True

else:

value = False

else:

value = type_(value_text)

setting[name] = value

return setting

class BacktesterChart(pg.GraphicsWindow):

""""""

def __init__(self):

""""""

super().__init__(title="Backtester Chart")

self.dates = {}

self.init_ui()

def init_ui(self):

""""""

pg.setConfigOptions(antialias=True)

# Create plot widgets

self.balance_plot = self.addPlot(

title="账户净值",

axisItems={"bottom": DateAxis(self.dates, orientation="bottom")}

)

self.nextRow()

self.drawdown_plot = self.addPlot(

title="净值回撤",

axisItems={"bottom": DateAxis(self.dates, orientation="bottom")}

)

self.nextRow()

self.pnl_plot = self.addPlot(

title="每日盈亏",

axisItems={"bottom": DateAxis(self.dates, orientation="bottom")}

)

self.nextRow()

self.distribution_plot = self.addPlot(title="盈亏分布")

# Add curves and bars on plot widgets

self.balance_curve = self.balance_plot.plot(

pen=pg.mkPen("#ffc107", width=3)

)

dd_color = "#303f9f"

self.drawdown_curve = self.drawdown_plot.plot(

fillLevel=-0.3, brush=dd_color, pen=dd_color

)

profit_color = 'r'

loss_color = 'g'

self.profit_pnl_bar = pg.BarGraphItem(

x=[], height=[], width=0.3, brush=profit_color, pen=profit_color

)

self.loss_pnl_bar = pg.BarGraphItem(

x=[], height=[], width=0.3, brush=loss_color, pen=loss_color

)

self.pnl_plot.addItem(self.profit_pnl_bar)

self.pnl_plot.addItem(self.loss_pnl_bar)

distribution_color = "#6d4c41"

self.distribution_curve = self.distribution_plot.plot(

fillLevel=-0.3, brush=distribution_color, pen=distribution_color

)

def clear_data(self):

""""""

self.balance_curve.setData([], [])

self.drawdown_curve.setData([], [])

self.profit_pnl_bar.setOpts(x=[], height=[])

self.loss_pnl_bar.setOpts(x=[], height=[])

self.distribution_curve.setData([], [])

def set_data(self, df):

""""""

if df is None:

return

count = len(df)

self.dates.clear()

for n, date in enumerate(df.index):

self.dates[n] = date

# Set data for curve of balance and drawdown

self.balance_curve.setData(df["balance"])

self.drawdown_curve.setData(df["drawdown"])

# Set data for daily pnl bar

profit_pnl_x = []

profit_pnl_height = []

loss_pnl_x = []

loss_pnl_height = []

for count, pnl in enumerate(df["net_pnl"]):

if pnl >= 0:

profit_pnl_height.append(pnl)

profit_pnl_x.append(count)

else:

loss_pnl_height.append(pnl)

loss_pnl_x.append(count)

self.profit_pnl_bar.setOpts(x=profit_pnl_x, height=profit_pnl_height)

self.loss_pnl_bar.setOpts(x=loss_pnl_x, height=loss_pnl_height)

# Set data for pnl distribution

hist, x = np.histogram(df["net_pnl"], bins="auto")

x = x[:-1]

self.distribution_curve.setData(x, hist)

class DateAxis(pg.AxisItem):

"""Axis for showing date data"""

def __init__(self, dates: dict, *args, **kwargs):

""""""

super().__init__(*args, **kwargs)

self.dates = dates

def tickStrings(self, values, scale, spacing):

""""""

strings = []

for v in values:

dt = self.dates.get(v, "")

strings.append(str(dt))

return strings

class OptimizationSettingEditor(QtWidgets.QDialog):

"""

For setting up parameters for optimization.

"""

DISPLAY_NAME_MAP = {

"总收益率": "total_return",

"夏普比率": "sharpe_ratio",

"收益回撤比": "return_drawdown_ratio",

"日均盈亏": "daily_net_pnl"

}

def __init__(

self, class_name: str, parameters: dict

):

""""""

super().__init__()

self.class_name = class_name

self.parameters = parameters

self.edits = {}

self.optimization_setting = None

self.use_ga = False

self.init_ui()

def init_ui(self):

""""""

QLabel = QtWidgets.QLabel

self.target_combo = QtWidgets.QComboBox()

self.target_combo.addItems(list(self.DISPLAY_NAME_MAP.keys()))

grid = QtWidgets.QGridLayout()

grid.addWidget(QLabel("目标"), 0, 0)

grid.addWidget(self.target_combo, 0, 1, 1, 3)

grid.addWidget(QLabel("参数"), 1, 0)

grid.addWidget(QLabel("开始"), 1, 1)

grid.addWidget(QLabel("步进"), 1, 2)

grid.addWidget(QLabel("结束"), 1, 3)

# Add vt_symbol and name edit if add new strategy

self.setWindowTitle(f"优化参数配置:{self.class_name}")

validator = QtGui.QDoubleValidator()

row = 2

for name, value in self.parameters.items():

type_ = type(value)

if type_ not in [int, float]:

continue

start_edit = QtWidgets.QLineEdit(str(value))

step_edit = QtWidgets.QLineEdit(str(1))

end_edit = QtWidgets.QLineEdit(str(value))

for edit in [start_edit, step_edit, end_edit]:

edit.setValidator(validator)

grid.addWidget(QLabel(name), row, 0)

grid.addWidget(start_edit, row, 1)

grid.addWidget(step_edit, row, 2)

grid.addWidget(end_edit, row, 3)

self.edits[name] = {

"type": type_,

"start": start_edit,

"step": step_edit,

"end": end_edit

}

row += 1

parallel_button = QtWidgets.QPushButton("多进程优化")

parallel_button.clicked.connect(self.generate_parallel_setting)

grid.addWidget(parallel_button, row, 0, 1, 4)

row += 1

ga_button = QtWidgets.QPushButton("遗传算法优化")

ga_button.clicked.connect(self.generate_ga_setting)

grid.addWidget(ga_button, row, 0, 1, 4)

widget = QtWidgets.QWidget()

widget.setLayout(grid)

scroll = QtWidgets.QScrollArea()

scroll.setWidgetResizable(True)

scroll.setWidget(widget)

vbox = QtWidgets.QVBoxLayout()

vbox.addWidget(scroll)

self.setLayout(vbox)

def generate_ga_setting(self):

""""""

self.use_ga = True

self.generate_setting()

def generate_parallel_setting(self):

""""""

self.use_ga = False

self.generate_setting()

def generate_setting(self):

""""""

self.optimization_setting = OptimizationSetting()

self.target_display = self.target_combo.currentText()

target_name = self.DISPLAY_NAME_MAP[self.target_display]

self.optimization_setting.set_target(target_name)

for name, d in self.edits.items():

type_ = d["type"]

start_value = type_(d["start"].text())

step_value = type_(d["step"].text())

end_value = type_(d["end"].text())

if start_value == end_value:

self.optimization_setting.add_parameter(name, start_value)

else:

self.optimization_setting.add_parameter(

name,

start_value,

end_value,

step_value

)

self.accept()

def get_setting(self):

""""""

return self.optimization_setting, self.use_ga

class OptimizationResultMonitor(QtWidgets.QDialog):

"""

For viewing optimization result.

"""

def __init__(

self, result_values: list, target_display: str

):

""""""

super().__init__()

self.result_values = result_values

self.target_display = target_display

self.init_ui()

def init_ui(self):

""""""

self.setWindowTitle("参数优化结果")

self.resize(1100, 500)

# Creat table to show result

table = QtWidgets.QTableWidget()

table.setColumnCount(2)

table.setRowCount(len(self.result_values))

table.setHorizontalHeaderLabels(["参数", self.target_display])

table.setEditTriggers(table.NoEditTriggers)

table.verticalHeader().setVisible(False)

table.horizontalHeader().setSectionResizeMode(

0, QtWidgets.QHeaderView.ResizeToContents

)

table.horizontalHeader().setSectionResizeMode(

1, QtWidgets.QHeaderView.Stretch

)

for n, tp in enumerate(self.result_values):

setting, target_value, _ = tp

setting_cell = QtWidgets.QTableWidgetItem(str(setting))

target_cell = QtWidgets.QTableWidgetItem(str(target_value))

setting_cell.setTextAlignment(QtCore.Qt.AlignCenter)

target_cell.setTextAlignment(QtCore.Qt.AlignCenter)

table.setItem(n, 0, setting_cell)

table.setItem(n, 1, target_cell)

# Create layout

button = QtWidgets.QPushButton("保存")

button.clicked.connect(self.save_csv)

hbox = QtWidgets.QHBoxLayout()

hbox.addStretch()

hbox.addWidget(button)

vbox = QtWidgets.QVBoxLayout()

vbox.addWidget(table)

vbox.addLayout(hbox)

self.setLayout(vbox)

def save_csv(self) -> None:

"""

Save table data into a csv file

"""

path, _ = QtWidgets.QFileDialog.getSaveFileName(

self, "保存数据", "", "CSV(*.csv)")

if not path:

return

with open(path, "w") as f:

writer = csv.writer(f, lineterminator="\n")

writer.writerow(["参数", self.target_display])

for tp in self.result_values:

setting, target_value, _ = tp

row_data = [str(setting), str(target_value)]

writer.writerow(row_data)

class BacktestingTradeMonitor(BaseMonitor):

"""

Monitor for backtesting trade data.

"""

headers = {

"tradeid": {"display": "成交号 ", "cell": BaseCell, "update": False},

"orderid": {"display": "委托号", "cell": BaseCell, "update": False},

"symbol": {"display": "代码", "cell": BaseCell, "update": False},

"exchange": {"display": "交易所", "cell": EnumCell, "update": False},

"direction": {"display": "方向", "cell": DirectionCell, "update": False},

"offset": {"display": "开平", "cell": EnumCell, "update": False},

"price": {"display": "价格", "cell": BaseCell, "update": False},

"volume": {"display": "数量", "cell": BaseCell, "update": False},

"datetime": {"display": "时间", "cell": BaseCell, "update": False},

"gateway_name": {"display": "接口", "cell": BaseCell, "update": False},

}

class BacktestingOrderMonitor(BaseMonitor):

"""

Monitor for backtesting order data.

"""

headers = {

"orderid": {"display": "委托号", "cell": BaseCell, "update": False},

"symbol": {"display": "代码", "cell": BaseCell, "update": False},

"exchange": {"display": "交易所", "cell": EnumCell, "update": False},

"type": {"display": "类型", "cell": EnumCell, "update": False},

"direction": {"display": "方向", "cell": DirectionCell, "update": False},

"offset": {"display": "开平", "cell": EnumCell, "update": False},

"price": {"display": "价格", "cell": BaseCell, "update": False},

"volume": {"display": "总数量", "cell": BaseCell, "update": False},

"traded": {"display": "已成交", "cell": BaseCell, "update": False},

"status": {"display": "状态", "cell": EnumCell, "update": False},

"datetime": {"display": "时间", "cell": BaseCell, "update": False},

"gateway_name": {"display": "接口", "cell": BaseCell, "update": False},

}

class DailyResultMonitor(BaseMonitor):

"""

Monitor for backtesting daily result.

"""

headers = {

"date": {"display": "日期", "cell": BaseCell, "update": False},

"trade_count": {"display": "成交笔数", "cell": BaseCell, "update": False},

"start_pos": {"display": "开盘持仓", "cell": BaseCell, "update": False},

"end_pos": {"display": "收盘持仓", "cell": BaseCell, "update": False},

"turnover": {"display": "成交额", "cell": BaseCell, "update": False},

"commission": {"display": "手续费", "cell": BaseCell, "update": False},

"slippage": {"display": "滑点", "cell": BaseCell, "update": False},

"trading_pnl": {"display": "交易盈亏", "cell": BaseCell, "update": False},

"holding_pnl": {"display": "持仓盈亏", "cell": BaseCell, "update": False},

"total_pnl": {"display": "总盈亏", "cell": BaseCell, "update": False},

"net_pnl": {"display": "净盈亏", "cell": BaseCell, "update": False},

}

class BacktestingResultDialog(QtWidgets.QDialog):

"""

"""

def __init__(

self,

main_engine: MainEngine,

event_engine: EventEngine,

title: str,

table_class: QtWidgets.QTableWidget

):

""""""

super().__init__()

self.main_engine = main_engine

self.event_engine = event_engine

self.title = title

self.table_class = table_class

self.updated = False

self.init_ui()

def init_ui(self):

""""""

self.setWindowTitle(self.title)

self.resize(1100, 600)

self.table = self.table_class(self.main_engine, self.event_engine)

vbox = QtWidgets.QVBoxLayout()

vbox.addWidget(self.table)

self.setLayout(vbox)

def clear_data(self):

""""""

self.updated = False

self.table.setRowCount(0)

def update_data(self, data: list):

""""""

self.updated = True

data.reverse()

for obj in data:

self.table.insert_new_row(obj)

def is_updated(self):

""""""

return self.updated

class CandleChartDialog(QtWidgets.QDialog):

"""

"""

def __init__(self):

""""""

super().__init__()

self.dt_ix_map = {}

self.dt_ix_map_min = {}

self.updated = False

self.init_ui()

def init_ui(self):

""""""

self.setWindowTitle("回测K线图表")

self.resize(1400, 800)

# Create chart widget

self.chart = ChartWidget()

self.chart.add_plot("candle", hide_x_axis=True)

self.chart.add_plot("volume", maximum_height=200)

self.chart.add_item(CandleItem, "candle", "candle")

self.chart.add_item(VolumeItem, "volume", "volume")

self.chart.add_cursor()

# Add scatter item for showing tradings

self.trade_scatter = pg.ScatterPlotItem()

candle_plot = self.chart.get_plot("candle")

candle_plot.addItem(self.trade_scatter)

# Set layout

vbox = QtWidgets.QVBoxLayout()

vbox.addWidget(self.chart)

self.setLayout(vbox)

def update_history(self, history: list):

""""""

self.updated = True

self.chart.update_history(history)

for ix, bar in enumerate(history):

self.dt_ix_map[bar.datetime] = ix

def update_trades(self, trades: list,show_min:int):

""""""

trade_data = []

for trade in trades:

ix = self.dt_ix_map_min[trade.datetime]

ix=ix//show_min

scatter = {

"pos": (ix, trade.price),

"data": 1,

"size": 14,

"pen": pg.mkPen((255, 255, 255))

}

if trade.direction == Direction.LONG:

scatter_symbol = "t1" # Up arrow

else:

scatter_symbol = "t" # Down arrow

if trade.offset == Offset.OPEN:

scatter_brush = pg.mkBrush((255, 255, 0)) # Yellow

else:

scatter_brush = pg.mkBrush((0, 0, 255)) # Blue

scatter["symbol"] = scatter_symbol

scatter["brush"] = scatter_brush

trade_data.append(scatter)

self.trade_scatter.setData(trade_data)

def clear_data(self):

""""""

self.updated = False

self.chart.clear_all()

self.dt_ix_map.clear()

self.trade_scatter.clear()

def is_updated(self):

""""""

return self.updated