1. algo应用和CTA应用增加用户策略方法不一样

- 新建CTA用户策略只要在 [用户命令]\strategies\目录下,创建自己的策略,实现on_start ,on_init, on_tick, on_bar, on_trade, on_order, on_stop_order等推送接口。重新加载cta app,vnpy系统会自动把系统自带策略和用户策略一起编译添加进CTA应用界面,直接选择就OK;

- algo应用却不是这样的,它的策略是在algo引擎初始化时候,执行load_algo_template()加载的,加载哪些策略是写死的,它没有像CTA app那样考虑用户策略的加载,代码如下:

def load_algo_template(self):

""""""

from .algos.twap_algo import TwapAlgo

from .algos.iceberg_algo import IcebergAlgo

from .algos.sniper_algo import SniperAlgo

from .algos.stop_algo import StopAlgo

from .algos.best_limit_algo import BestLimitAlgo

from .algos.grid_algo import GridAlgo

from .algos.dma_algo import DmaAlgo

from .algos.arbitrage_algo import ArbitrageAlgo

from .algos.test_algo import TestAlgo # hxxjava add

self.add_algo_template(TwapAlgo)

self.add_algo_template(IcebergAlgo)

self.add_algo_template(SniperAlgo)

self.add_algo_template(StopAlgo)

self.add_algo_template(BestLimitAlgo)

self.add_algo_template(GridAlgo)

self.add_algo_template(DmaAlgo)

self.add_algo_template(ArbitrageAlgo)

self.add_algo_template(TestAlgo) # hxxjava add

from .genus import (

GenusVWAP,

GenusTWAP,

GenusPercent,

GenusPxInline,

GenusSniper,

GenusDMA

)

self.add_algo_template(GenusVWAP)

self.add_algo_template(GenusTWAP)

self.add_algo_template(GenusPercent)

self.add_algo_template(GenusPxInline)

self.add_algo_template(GenusSniper)

self.add_algo_template(GenusDMA)考虑到这一特点,只能像上面带注释的行这么添加algo策略。

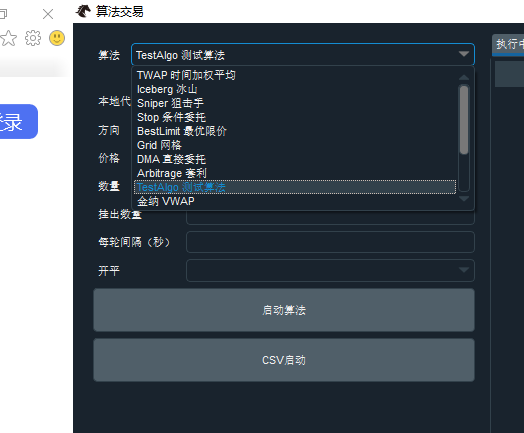

2. 复制Iceberg策略代码,修改成TestAlgo策略

from vnpy.trader.constant import Offset, Direction

from vnpy.trader.object import TradeData, OrderData, TickData

from vnpy.trader.engine import BaseEngine

from vnpy.app.algo_trading import AlgoTemplate

class TestAlgo(AlgoTemplate):

""""""

display_name = "TestAlgo 测试算法"

default_setting = {

"vt_symbol": "",

"direction": [Direction.LONG.value, Direction.SHORT.value],

"price": 0.0,

"volume": 0.0,

"display_volume": 0.0,

"interval": 0,

"offset": [

Offset.NONE.value,

Offset.OPEN.value,

Offset.CLOSE.value,

Offset.CLOSETODAY.value,

Offset.CLOSEYESTERDAY.value

]

}

variables = [

"traded",

"timer_count",

"vt_orderid"

]

def __init__(

self,

algo_engine: BaseEngine,

algo_name: str,

setting: dict

):

""""""

super().__init__(algo_engine, algo_name, setting)

# Parameters

self.vt_symbol = setting["vt_symbol"]

self.direction = Direction(setting["direction"])

self.price = setting["price"]

self.volume = setting["volume"]

self.display_volume = setting["display_volume"]

self.interval = setting["interval"]

self.offset = Offset(setting["offset"])

# Variables

self.timer_count = 0

self.vt_orderid = ""

self.traded = 0

self.last_tick = None

self.subscribe(self.vt_symbol)

self.put_parameters_event()

self.put_variables_event()

def on_stop(self):

""""""

self.write_log("停止算法")

def on_tick(self, tick: TickData):

""""""

self.last_tick = tick

def on_order(self, order: OrderData):

""""""

msg = f"委托号:{order.vt_orderid},委托状态:{order.status.value}"

self.write_log(msg)

if not order.is_active():

self.vt_orderid = ""

self.put_variables_event()

def on_trade(self, trade: TradeData):

""""""

self.traded += trade.volume

if self.traded >= self.volume:

self.write_log(f"已交易数量:{self.traded},总数量:{self.volume}")

self.stop()

else:

self.put_variables_event()

def on_timer(self):

""""""

self.timer_count += 1

if self.timer_count < self.interval:

self.put_variables_event()

return

self.timer_count = 0

contract = self.get_contract(self.vt_symbol)

if not contract:

return

print(f"last_tick={self.last_tick}")

# # If order already finished, just send new order

# if not self.vt_orderid:

# order_volume = self.volume - self.traded

# order_volume = min(order_volume, self.display_volume)

# if self.direction == Direction.LONG:

# self.vt_orderid = self.buy(

# self.vt_symbol,

# self.price,

# order_volume,

# offset=self.offset

# )

# else:

# self.vt_orderid = self.sell(

# self.vt_symbol,

# self.price,

# order_volume,

# offset=self.offset

# )

# # Otherwise check for cancel

# else:

# if self.direction == Direction.LONG:

# if self.last_tick.ask_price_1 <= self.price:

# self.cancel_order(self.vt_orderid)

# self.vt_orderid = ""

# self.write_log(u"最新Tick卖一价,低于买入委托价格,之前委托可能丢失,强制撤单")

# else:

# if self.last_tick.bid_price_1 >= self.price:

# self.cancel_order(self.vt_orderid)

# self.vt_orderid = ""

# self.write_log(u"最新Tick买一价,高于卖出委托价格,之前委托可能丢失,强制撤单")

self.put_variables_event()3. 重新启动algo就可以看见 ”TestAlgo 测试算法“啦