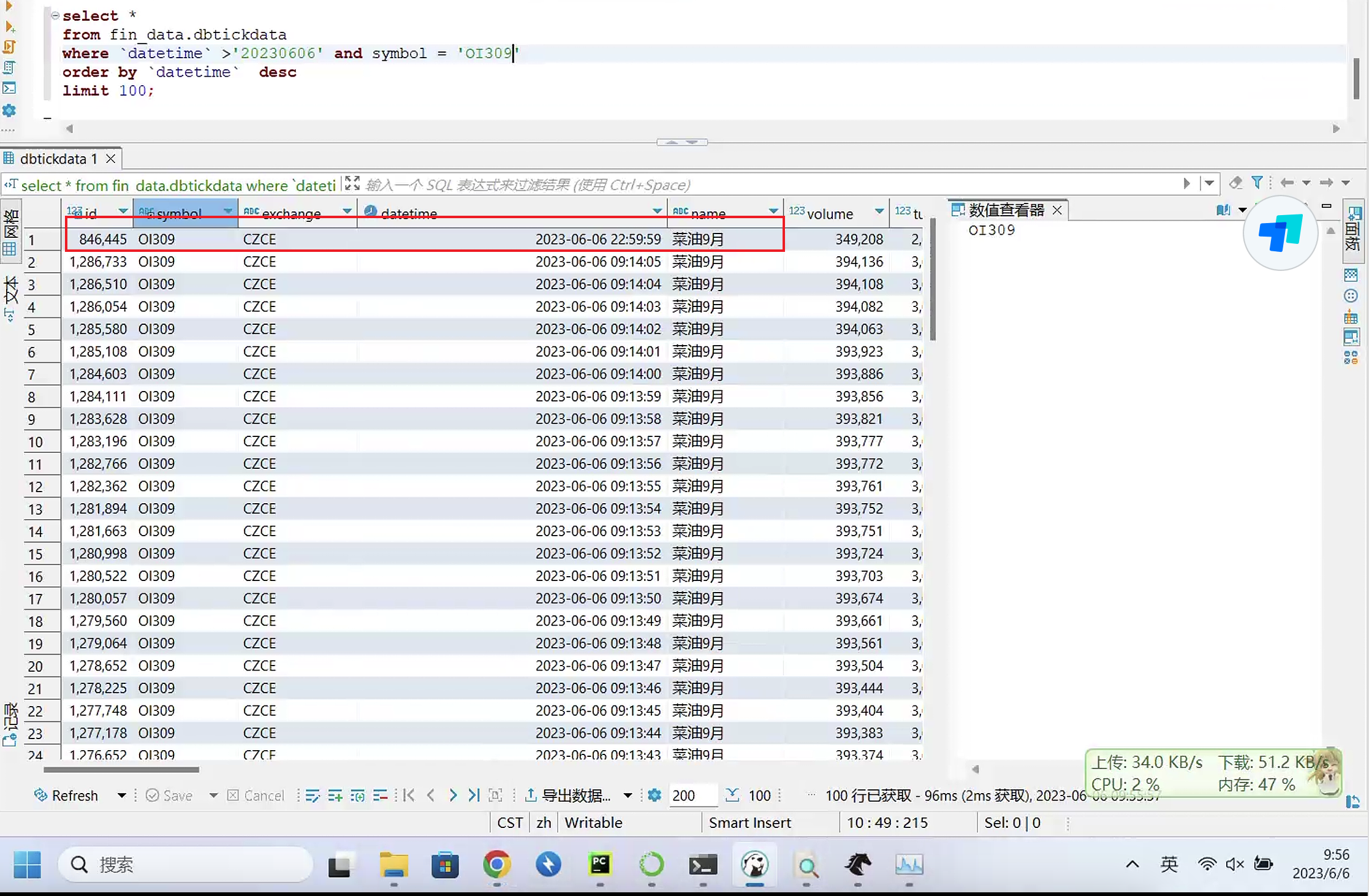

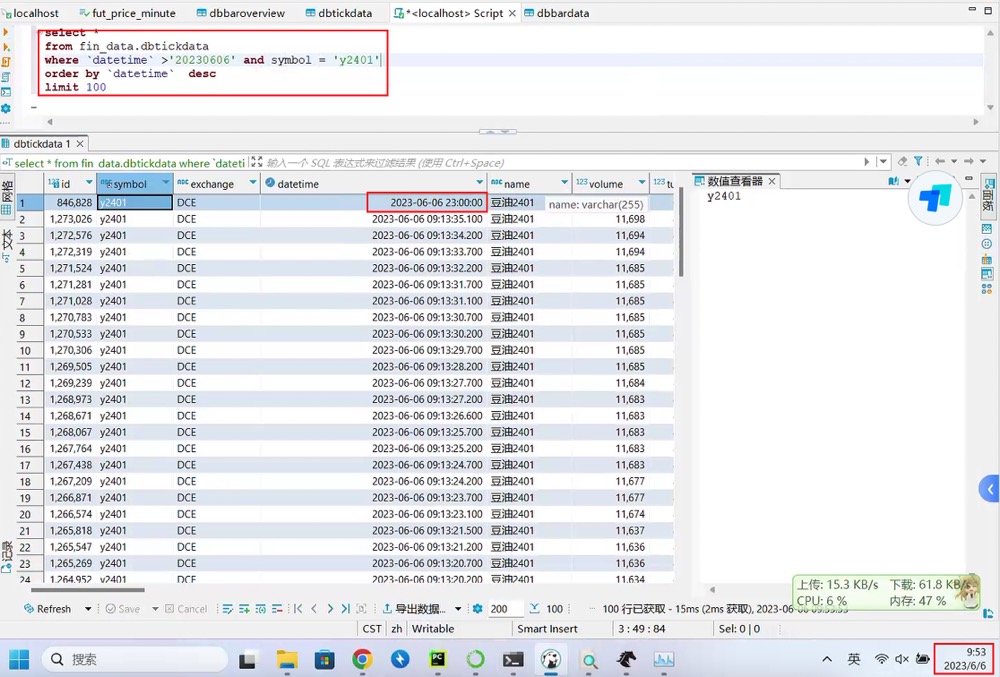

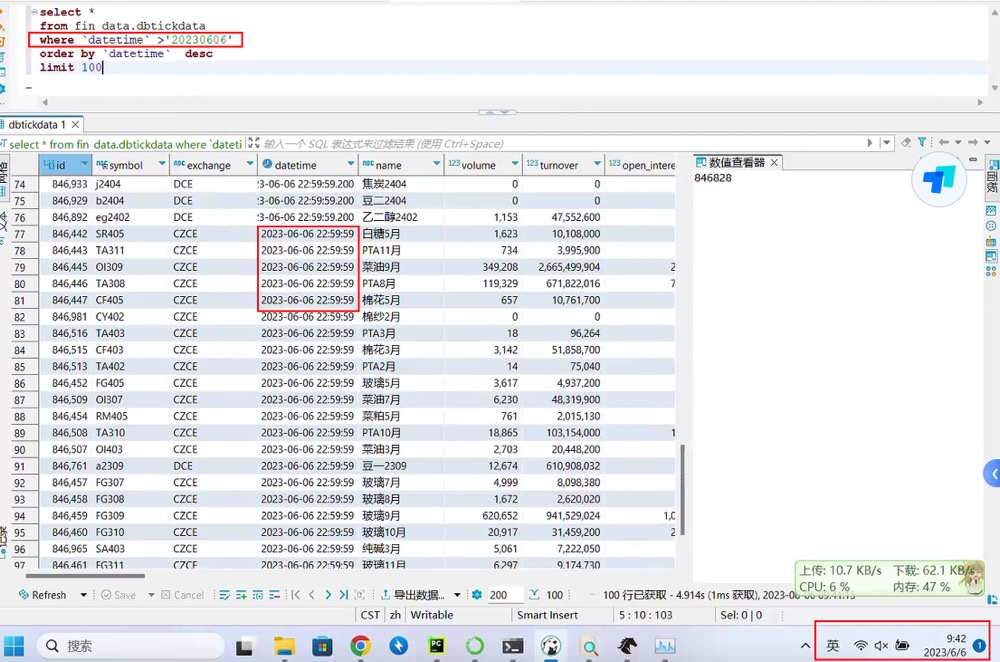

无意间发现tick行情录制会出现当天晚上11点的数据,请问各位大佬是什么原因呢。我用的行情录制的代码是本论坛提供的

import sys

import multiprocessing

import re

from copy import copy

from vnpy.trader.constant import Exchange

from vnpy.trader.object import BarData, TickData

from enum import Enum

from time import sleep

from datetime import datetime, time

from logging import INFO

from vnpy.event import EventEngine

from vnpy.trader.setting import SETTINGS

from vnpy.trader.engine import MainEngine

from vnpy.trader.utility import load_json, extract_vt_symbol

from vnpy_ctp import CtpGateway

from vnpy_ctastrategy.base import EVENT_CTA_LOG

from vnpy_datarecorder.engine import RecorderEngine

EXCHANGE_LIST = [

Exchange.SHFE,

Exchange.DCE,

Exchange.CZCE,

Exchange.CFFEX,

Exchange.INE,

]

SETTINGS["log.active"] = True

SETTINGS["log.level"] = INFO

SETTINGS["log.console"] = True

CTP_SETTING = load_json("connect_ctp.json")

def is_futures(vt_symbol: str) -> bool:

"""

是否是期货

"""

return bool(re.match(r"^[a-zA-Z]{1,3}\d{2,4}.[A-Z]+$", vt_symbol))

class RecordMode(Enum):

BAR = "bar"

TICK = "tick"

class WholeMarketRecorder(RecorderEngine):

def __init__(self, main_engine, event_engine, record_modes=[RecordMode.BAR,RecordMode.TICK]):

super().__init__(main_engine, event_engine)

self.record_modes = record_modes

# 非交易时间

self.drop_start = time(3, 15)

self.drop_end = time(8, 45)

# 大连、上海、郑州交易所,小节休息

self.rest_start = time(10, 15)

self.rest_end = time(10, 30)

def is_trading(self, vt_symbol, current_time) -> bool:

"""

交易时间,过滤校验Tick

"""

symbol, exchange = extract_vt_symbol(vt_symbol)

if current_time >= self.drop_start and current_time < self.drop_end:

return False

if exchange in [Exchange.DCE, Exchange.SHFE, Exchange.CZCE]:

if current_time >= self.rest_start and current_time < self.rest_end:

return False

return True

def record_tick(self, tick: TickData):

"""

抛弃非交易时间校验数据

"""

tick_time = tick.datetime.time()

if not self.is_trading(tick.vt_symbol, tick_time):

return

task = ("tick", [copy(tick)])

self.queue.put(task)

def record_bar(self, bar: BarData):

"""

抛弃非交易时间校验数据

"""

bar_time = bar.datetime.time()

if not self.is_trading(bar.vt_symbol, bar_time):

return

print("push")

print(bar)

task = ("bar", [copy(bar)])

self.queue.put(task)

def load_setting(self):

# 不读取原数据记录设置

pass

def process_contract_event(self, event):

"""

设置记录所有期货合约

"""

contract = event.data

vt_symbol = contract.vt_symbol

# 不录制期权

if is_futures(vt_symbol):

if RecordMode.BAR in self.record_modes:

self.add_bar_recording(vt_symbol)

if RecordMode.TICK in self.record_modes:

self.add_tick_recording(vt_symbol)

self.subscribe(contract)

def run_child():

"""

Running in the child process.

"""

SETTINGS["log.file"] = True

event_engine = EventEngine()

main_engine = MainEngine(event_engine)

main_engine.add_gateway(CtpGateway)

main_engine.write_log("主引擎创建成功")

# 记录引擎

log_engine = main_engine.get_engine("log")

event_engine.register(EVENT_CTA_LOG, log_engine.process_log_event)

main_engine.write_log("注册日志事件监听")

main_engine.connect(CTP_SETTING, "CTP")

main_engine.write_log("连接CTP接口")

whole_market_recorder = WholeMarketRecorder(main_engine, event_engine)

main_engine.write_log("开始录制数据")

# oms_engine = main_engine.get_engine("oms")

while True:

sleep(1)

def run_parent():

"""

Running in the parent process.

"""

print("启动CTA策略守护父进程")

# Chinese futures market trading period (day/night)

MORNING_START = time(8, 45)

MORNING_END = time(11, 45)

AFTERNOON_START = time(13, 15)

AFTERNOON_END = time(15, 15)

NIGHT_START = time(20, 45)

NIGHT_END = time(2, 45)

child_process = None

while True:

current_time = datetime.now().time()

trading = False

# Check whether in trading period

if (

(current_time >= MORNING_START and current_time <= MORNING_END)

or (current_time >= AFTERNOON_START and current_time <= AFTERNOON_END)

or (current_time >= NIGHT_START)

or (current_time <= NIGHT_END)

):

trading = True

# Start child process in trading period

if trading and child_process is None:

print("启动数据录制子进程")

child_process = multiprocessing.Process(target=run_child)

child_process.start()

print("数据录制子进程启动成功")

# 非记录时间则退出数据录制子进程

if not trading and child_process is not None:

print("关闭数据录制子进程")

child_process.terminate()

child_process.join()

child_process = None

print("数据录制子进程关闭成功")

sys.stdout.flush()

sleep(5)

if __name__ == "__main__":

run_parent()