现在VeighNa交易是按日进行统计回测的,但是在之前的v1版本,是同时支持按日和按照交易数统计回测结果。

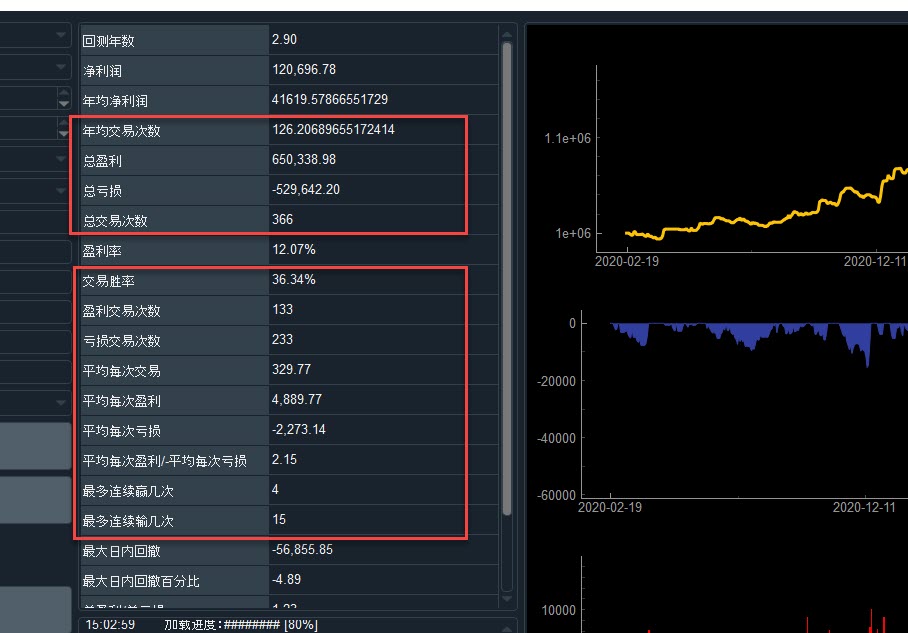

通过借用之前版本的代码,可以获得按交易数统计回测结果,下图示例,其中红框的都是按交易统计获得数据,比如交易胜率就是盈利交易次数比总交易次数:

代码改动,在cta_strategy.backtesting新增TradingResult类中,这里如果输入费率如果大于0.1,则费率按手数计算,小于按照保证金百分比计算。

class TradingResult:

"""每笔交易的结果"""

#----------------------------------------------------------------------

def __init__(self, entryPrice, entryDt, exitPrice,

exitDt, volume, rate, slippage, size):

"""Constructor"""

self.entryPrice = entryPrice # 开仓价格

self.exitPrice = exitPrice # 平仓价格

self.entryDt = entryDt # 开仓时间datetime

self.exitDt = exitDt # 平仓时间

self.volume = volume # 交易数量(+/-代表方向)

self.turnover = (self.entryPrice+self.exitPrice)*size*abs(volume) # 成交金额

if rate < 0.1:

self.commission = self.turnover*rate # 手续费成本

else:

self.commission = abs(volume)*rate*2

self.slippage = slippage*2*size*abs(volume) # 滑点成本

self.pnl = ((self.exitPrice - self.entryPrice) * volume * size

- self.commission - self.slippage) # 净盈亏代码改动,在cta_strategy.backtesting的BacktestingEngine类中,其实这段代码基本就是1.92 copy过来,稍微改改。

#----------------------------------------------------------------------

def calculateBacktestingResult(self):

"""

计算回测结果

"""

self.output(u'计算回测结果')

# 检查成交记录

if not self.trades:

self.output(u'成交记录为空,无法计算回测结果')

noResult = {}

noResult['capital'] = 0

noResult['maxCapital'] = 0

noResult['drawdown'] = 0

noResult['totalResult'] = 0

noResult['totalTurnover'] = 0

noResult['totalCommission'] = 0

noResult['totalSlippage'] = 0

noResult['timeList'] = 0

noResult['pnlList'] = 0

noResult['capitalList'] = 0

noResult['drawdownList'] = 0

noResult['winningRate'] = 0

noResult['averageWinning'] = 0

noResult['averageLosing'] = 0

noResult['profitLossRatio'] = 0

noResult['posList'] = 0

noResult['tradeTimeList'] = 0

noResult['resultList'] = 0

noResult['maxDrawdown'] = 0

return noResult

# 首先基于回测后的成交记录,计算每笔交易的盈亏

resultList = [] # 交易结果列表

longTrade = [] # 未平仓的多头交易

shortTrade = [] # 未平仓的空头交易

tradeTimeList = [] # 每笔成交时间戳

posList = [0] # 每笔成交后的持仓情况

for trade in self.trades.values():

# 复制成交对象,因为下面的开平仓交易配对涉及到对成交数量的修改

# 若不进行复制直接操作,则计算完后所有成交的数量会变成0

trade = copy.copy(trade)

# 多头交易

if trade.direction == Direction.LONG:

# 如果尚无空头交易

if not shortTrade:

longTrade.append(trade)

# 当前多头交易为平空

else:

while True:

entryTrade = shortTrade[0]

exitTrade = trade

# 清算开平仓交易

closedVolume = min(exitTrade.volume, entryTrade.volume)

result = TradingResult(entryTrade.price, entryTrade.datetime,

exitTrade.price, exitTrade.datetime,

-closedVolume, self.rate, self.slippage, self.size)

resultList.append(result)

posList.extend([-1, 0])

tradeTimeList.extend([result.entryDt, result.exitDt])

# 计算未清算部分

entryTrade.volume -= closedVolume

exitTrade.volume -= closedVolume

# 如果开仓交易已经全部清算,则从列表中移除

if not entryTrade.volume:

shortTrade.pop(0)

# 如果平仓交易已经全部清算,则退出循环

if not exitTrade.volume:

break

# 如果平仓交易未全部清算,

if exitTrade.volume:

# 且开仓交易已经全部清算完,则平仓交易剩余的部分

# 等于新的反向开仓交易,添加到队列中

if not shortTrade:

longTrade.append(exitTrade)

break

# 如果开仓交易还有剩余,则进入下一轮循环

else:

pass

# 空头交易

else:

# 如果尚无多头交易

if not longTrade:

shortTrade.append(trade)

# 当前空头交易为平多

else:

while True:

entryTrade = longTrade[0]

exitTrade = trade

# 清算开平仓交易

closedVolume = min(exitTrade.volume, entryTrade.volume)

result = TradingResult(entryTrade.price, entryTrade.datetime,

exitTrade.price, exitTrade.datetime,

closedVolume, self.rate, self.slippage, self.size)

resultList.append(result)

posList.extend([1, 0])

tradeTimeList.extend([result.entryDt, result.exitDt])

# 计算未清算部分

entryTrade.volume -= closedVolume

exitTrade.volume -= closedVolume

# 如果开仓交易已经全部清算,则从列表中移除

if not entryTrade.volume:

longTrade.pop(0)

# 如果平仓交易已经全部清算,则退出循环

if not exitTrade.volume:

break

# 如果平仓交易未全部清算,

if exitTrade.volume:

# 且开仓交易已经全部清算完,则平仓交易剩余的部分

# 等于新的反向开仓交易,添加到队列中

if not longTrade:

shortTrade.append(exitTrade)

break

# 如果开仓交易还有剩余,则进入下一轮循环

else:

pass

# 到最后交易日尚未平仓的交易,则以最后价格平仓

if self.mode == BacktestingMode.BAR:

endPrice = self.bar.close_price

else:

endPrice = self.tick.last_price

for trade in longTrade:

result = TradingResult(trade.price, trade.datetime, endPrice, self.datetime,

trade.volume, self.rate, self.slippage, self.size)

resultList.append(result)

for trade in shortTrade:

result = TradingResult(trade.price, trade.datetime, endPrice, self.datetime,

-trade.volume, self.rate, self.slippage, self.size)

resultList.append(result)

# 检查是否有交易

if not resultList:

self.output(u'无交易结果')

return {}

# 然后基于每笔交易的结果,我们可以计算具体的盈亏曲线和最大回撤等

capital = 0 # 资金

maxCapital = 0 # 资金最高净值

drawdown = 0 # 回撤

totalResult = 0 # 总成交数量

totalTurnover = 0 # 总成交金额(合约面值)

totalCommission = 0 # 总手续费

totalSlippage = 0 # 总滑点

timeList = [] # 时间序列

pnlList = [] # 每笔盈亏序列

capitalList = [] # 盈亏汇总的时间序列

drawdownList = [] # 回撤的时间序列

winningResult = 0 # 盈利次数

losingResult = 0 # 亏损次数

totalWinning = 0 # 总盈利金额

totalLosing = 0 # 总亏损金额

maxDrawdown = 0 # 最大回撤

max_win_count = 0

win_count = 0

max_lose_count = 0

lose_count = 0

for result in resultList:

capital += result.pnl

maxCapital = max(capital, maxCapital)

drawdown = capital - maxCapital

maxDrawdown = min(drawdown, maxDrawdown)

pnlList.append(result.pnl)

timeList.append(result.exitDt) # 交易的时间戳使用平仓时间

capitalList.append(capital)

drawdownList.append(drawdown)

totalResult += 1

totalTurnover += result.turnover

totalCommission += result.commission

totalSlippage += result.slippage

if result.pnl >= 0:

winningResult += 1

totalWinning += result.pnl

max_lose_count = max(max_lose_count, lose_count)

lose_count = 0

win_count +=1

else:

losingResult += 1

totalLosing += result.pnl

max_win_count = max(max_win_count, win_count)

win_count = 0

lose_count +=1

# 计算盈亏相关数据

winningRate = winningResult / totalResult * 100 # 胜率

averageWinning = 0 # 这里把数据都初始化为0

averageLosing = 0

profitLossRatio = 0

if winningResult:

averageWinning = totalWinning / winningResult # 平均每笔盈利

if losingResult:

averageLosing = totalLosing / losingResult # 平均每笔亏损

if averageLosing:

profitLossRatio = -averageWinning / averageLosing # 盈亏比

#shaperadio

annualDays =240

dailyReturn = np.mean(pnlList) * 100

returnStd = np.std(pnlList) * 100

if returnStd:

sharpeRatio = dailyReturn / returnStd

else:

sharpeRatio = 0

# 返回回测结果

d = {}

d['capital'] = capital

d['maxCapital'] = maxCapital

d['drawdown'] = drawdown

d['totalResult'] = totalResult

d['totalTurnover'] = totalTurnover

d['totalCommission'] = totalCommission

d['totalSlippage'] = totalSlippage

d['timeList'] = timeList

d['pnlList'] = pnlList

d['capitalList'] = capitalList

d['drawdownList'] = drawdownList

d["averageProfit"] = capital/totalResult

d['winningRate'] = winningRate

d["totalWinning"] = totalWinning

d["winningResult"] = winningResult

d['averageWinning'] = averageWinning

d["totalLosing"] = totalLosing

d["losingResult"] = losingResult

d['averageLosing'] = averageLosing

d['profitLossRatio'] = profitLossRatio

d['posList'] = posList

d['tradeTimeList'] = tradeTimeList

d['resultList'] = resultList

d['maxDrawdown'] = maxDrawdown

d['sharpeRatio'] = sharpeRatio

d['returnStd'] = returnStd

d['max_win_count'] = max_win_count

d['max_lose_count'] = max_lose_count

return d使用也很简单,BacktestingEngine在run_backtesting 后, 运行calculateBacktestingResult,可以返回一个Dict,带着相关按次数分析的回测结果。