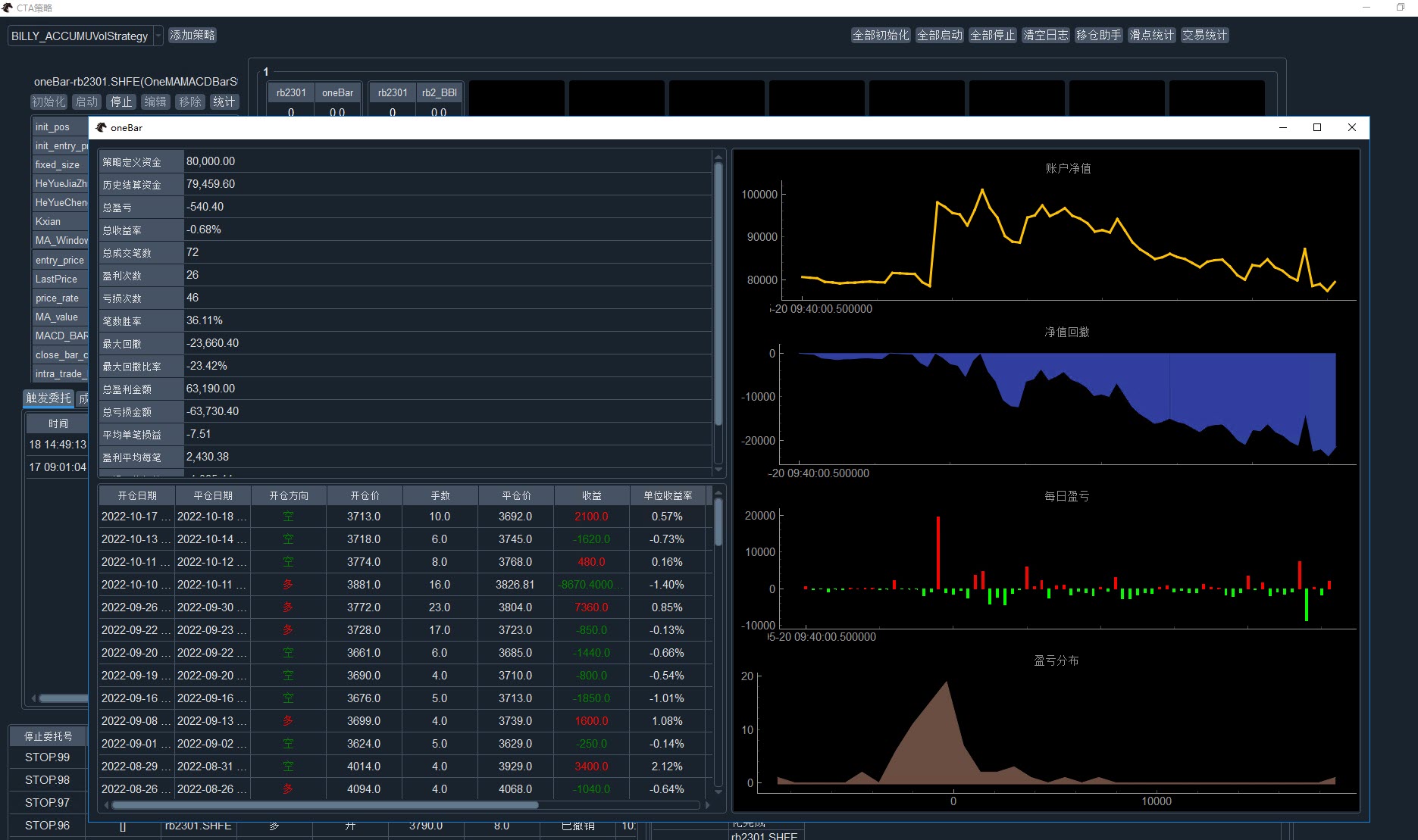

利用之前文章写的保存成交order,借鉴vnpy已有的回测分析报表,生成一个实盘交易分析报表。

截图如下。

这里有个统计按钮,点击输出统计界面

因为我的代码改动不少,直接拿来用估计不合适,只做参考。

首先要自行修改database的代码,新增按照strategy名称,和时间段读取保存到数据的order,按照时许正向返回。

读取出来是一个order的队列,下面代码可以放在cta_engine.py, 是把开仓价和开仓时间作为属性附加到平仓单,输出平仓单队列。对于没有成对的,或者跨期的品种配对要抛弃;这里在做移仓操作时候,要针对策略,生成虚拟的平仓和开新仓的订单,具体实现代码后面再移仓代码中说。

def convert_strategy_triggered_order(self,strategy_name,open_date = datetime(2001,10,10), close_date = datetime(2100,10,10)):

result = database_manager.load_triggered_stop_order_data(strategy_name,open_date,close_date)

if result:

matchedOrderList = []

last_order = None

for order in result:

if order.offset == Offset.OPEN:

last_order = copy(order)

elif last_order != None and order.offset == Offset.CLOSE:

if last_order.vt_symbol != order.vt_symbol:

last_order = None

continue

order.open_datetime= last_order.datetime

order.open_price = last_order.average_price

matchedOrderList.append(copy(order))

last_order = None

return matchedOrderList然后下面代码是处理的平仓单队列进行分析,计算出各种指标,输出为DataFrame格式,这里包括收益金额,收益率,单位收益率,回撤,账面价值等。

def get_strategy_triggered_order(self,strategy_name):

# result = database_manager.load_close_triggered_stop_order_data(strategy_name)

result = self.convert_strategy_triggered_order(strategy_name)

objectDF = DataFrame(data=None,columns=["开仓日期","平仓日期", "开仓方向", "开仓价", "手数", "平仓价", "收益"],dtype=object)

if result:

parameters = self.get_strategy_parameters(strategy_name)

# 策略中定义的合约价值

HeYueJiaZhi = parameters["HeYueJiaZhi"]

# 策略中定义的品种每笔数量

HeYueChengShu = parameters["HeYueChengShu"]

for close_data in result:

if close_data.direction == Direction.LONG:

close_data.direction = Direction.SHORT

else:

close_data.direction = Direction.LONG

objectDF.loc[len(objectDF) + 1] = [close_data.vt_orderids[0].replace(tzinfo=None),close_data.datetime.replace(tzinfo=None), close_data.direction, close_data.open_price,close_data.volume, close_data.average_price,0.0]

objectDF["收益"] = objectDF.apply(lambda x: x['开仓价'] - x['平仓价'] if x['开仓方向'] == Direction.SHORT else x['平仓价'] - x['开仓价'],

axis=1)

objectDF["UnitReturn"] = objectDF["收益"] * 100 / objectDF['开仓价']

objectDF["收益"] = objectDF["收益"]*HeYueChengShu*objectDF["手数"]

objectDF["balance"] = objectDF["收益"].cumsum() + HeYueJiaZhi

objectDF["return"] = objectDF["收益"]*100/HeYueJiaZhi

objectDF.loc[0] = copy(objectDF.iloc[0])

objectDF = objectDF.sort_index()

objectDF.loc[0,"balance"] = HeYueJiaZhi

objectDF["highlevel"] = (

objectDF["balance"].rolling(

min_periods=1, window=len(objectDF), center=False).max()

)

objectDF.drop(index=0, inplace=True)

objectDF["drawdown"] = objectDF["balance"] - objectDF["highlevel"]

objectDF["ddpercent"] = objectDF["drawdown"] / objectDF["highlevel"] * 100

return objectDF下面代码是分析dataframe,计算指标数据

def calculate_statistics(self, objectDF):

"""

"""

data = {}

# end_balance = df["balance"].iloc[-1]

# max_drawdown = df["drawdown"].min()

# max_ddpercent = df["ddpercent"].min()

HeYueJiaZhi = self._data["parameters"]["HeYueJiaZhi"]

data["capital"] = HeYueJiaZhi

data["total_net_pnl"] = objectDF["收益"].sum()

data["end_balance"] = objectDF["balance"].iloc[-1]

data["total_return"] = data["total_net_pnl"]*100/max(HeYueJiaZhi,1)

data["max_drawdown"] = objectDF["drawdown"].min()

data["max_ddpercent"] = objectDF["ddpercent"].min()

data["total_trade_count"] = len(objectDF)

data["winningResult"] = len(objectDF[objectDF["收益"] >0])

data["losingResult"] = len(objectDF[objectDF["收益"] <0])

data["winningRate"] = data["winningResult"] *100/ data["total_trade_count"]

data["totalWinning"] = objectDF[objectDF["收益"] >0]["收益"].sum()

data["totalLosing"] = objectDF[objectDF["收益"] <0]["收益"].sum()

data["averageWinning"] = data["totalWinning"]/max(1,data["winningResult"])

data["averageLosing"] = data["totalLosing"]/max(1,data["losingResult"])

data["perprofitLoss"] = data["total_net_pnl"] / data["total_trade_count"]

data["profitLossRatio"] = data["averageWinning"] / max(1,abs(data["averageLosing"]))

return data然后在cta_widget.py 中,加入显示代码,这里直接使用回撤模块的BacktesterChart

def analyze_strategy(self):

objectDF = self.cta_engine.get_strategy_triggered_order(self.strategy_name)

if not objectDF.empty:

triggerd_statistics_monitor = Triggered_OrderStatisticsMonitor()

triggerd_statistics_monitor.set_data(self.calculate_statistics(objectDF))

triggerd_statistics_monitor.setMinimumHeight(400)

triggerd_view = TriggeredMonitor(self.cta_manager.main_engine, self.cta_manager.main_engine.event_engine)

triggerd_view.set_df(objectDF)

triggerd_view.setMinimumHeight(400)

triggerd_view.setMinimumWidth(600)

objectDF["net_pnl"] = objectDF["收益"]

objectDF= objectDF.set_index("平仓日期")

chart = BacktesterChart()

chart.set_data(objectDF)

analyz_dialog = QDialog()

analyz_dialog.setWindowTitle(self.strategy_name)

analyz_dialog.setWindowModality(Qt.NonModal)

analyz_dialog.setWindowFlags(Qt.Dialog | Qt.WindowMinMaxButtonsHint | Qt.WindowCloseButtonHint)

gbox = QtWidgets.QGridLayout()

analyz_dialog.resize(1200, 800)

gbox.addWidget(triggerd_statistics_monitor,0,0)

gbox.addWidget(triggerd_view,1,0)

gbox.addWidget(chart,0,1,2,1)

analyz_dialog.setLayout(gbox)

analyz_dialog.exec_()

class PercentCell(BaseCell):

def __init__(self, content: Any, data: Any):

super(PercentCell, self).__init__(content, data)

def set_content(self, content: Any, data: Any) -> None:

self.setText(f"{content:,.2f}%")

self._data = data

class fullDatetimeCell(BaseCell):

def __init__(self, content: Any, data: Any):

super(fullDatetimeCell, self).__init__(content, data)

def set_content(self, content: Any, data: Any) -> None:

if content is None:

return

timestamp = content.strftime("%Y%m%d %H:%M:%S")

self.setText(timestamp)

self._data = data

class TriggeredMonitor(BaseMonitor):

event_type = ""

data_key = ""

sorting = False

# ["平仓日期", "方向", "开仓价", "手数", "平仓价", "收益"]

headers = {

"开仓日期": {"display": "开仓日期", "cell": fullDatetimeCell, "update": False},

"平仓日期": {"display": "平仓日期", "cell": fullDatetimeCell, "update": False},

"开仓方向": {"display": "开仓方向", "cell": DirectionCell, "update": False},

"开仓价": {"display": "开仓价", "cell": BaseCell, "update": False},

"手数": {"display": "手数", "cell": BaseCell, "update": False},

"平仓价": {"display": "平仓价", "cell": BaseCell, "update": False},

"收益": {"display": "收益", "cell": PnlCell, "update": False},

"return": {"display": "收益率", "cell": PercentCell, "update": False},

"UnitReturn": {"display": "单位收益率", "cell": PercentCell, "update": False},

"balance": {"display": "当前资金", "cell": BaseCell, "update": False},

"drawdown": {"display": "回撤", "cell": BaseCell, "update": False}

}

def set_df(self,objectDF):

objectDF_list = objectDF.to_dict(orient='records')

for record_item in objectDF_list:

self.insert_data(record_item)

def insert_data(self, data):

self.insertRow(0)

for column, header in enumerate(self.headers.keys()):

setting = self.headers[header]

content = data[header]

cell = setting["cell"](content, data)

self.setItem(0, column, cell)

def __del__(self) -> None:

pass

class Triggered_OrderStatisticsMonitor(QtWidgets.QTableWidget):

KEY_NAME_MAP = {

"capital": "策略定义资金",

"end_balance": "历史结算资金",

"total_net_pnl": "总盈亏",

"total_return": "总收益率",

"total_trade_count": "总成交笔数",

"winningResult": "盈利次数",

"losingResult" : "亏损次数",

"winningRate": "笔数胜率",

"max_drawdown": "最大回撤",

"max_ddpercent": "最大回撤比率",

"totalWinning": "总盈利金额",

"totalLosing": "总亏损金额",

"perprofitLoss": "平均单笔损益",

"averageWinning": "盈利平均每笔",

"averageLosing" : "亏损平均每笔",

"profitLossRatio" : "盈亏比",

}

def __init__(self):

super().__init__()

self.cells = {}

self.init_ui()

def init_ui(self):

self.setRowCount(len(self.KEY_NAME_MAP))

self.setVerticalHeaderLabels(list(self.KEY_NAME_MAP.values()))

self.setColumnCount(1)

self.horizontalHeader().setVisible(False)

self.horizontalHeader().setSectionResizeMode(

QtWidgets.QHeaderView.Stretch

)

self.setEditTriggers(self.NoEditTriggers)

for row, key in enumerate(self.KEY_NAME_MAP.keys()):

cell = QtWidgets.QTableWidgetItem()

self.setItem(row, 0, cell)

self.cells[key] = cell

def clear_data(self):

for cell in self.cells.values():

cell.setText("")

def set_data(self, data: dict):

data["capital"] = f"{data['capital']:,.2f}"

data["end_balance"] = f"{data['end_balance']:,.2f}"

data["total_net_pnl"] = f"{data['total_net_pnl']:,.2f}"

data["total_return"] = f"{data['total_return']:,.2f}%"

data["total_trade_count"] = f"{data['total_trade_count']}"

data["winningResult"] = f"{data['winningResult']}"

data["losingResult"] = f"{data['losingResult']}"

data["winningRate"] = f"{data['winningRate']:,.2f}%"

data["max_drawdown"] = f"{data['max_drawdown']:,.2f}"

data["max_ddpercent"] = f"{data['max_ddpercent']:,.2f}%"

data["totalWinning"] = f"{data['totalWinning']:,.2f}"

data["totalLosing"] = f"{data['totalLosing']:,.2f}"

data["averageWinning"] = f"{data['averageWinning']:,.2f}"

data["averageLosing"] = f"{data['averageLosing']:,.2f}"

data["perprofitLoss"] = f"{data['perprofitLoss']:,.2f}"

data["profitLossRatio"] = f"{data['profitLossRatio']:,.2f}"

for key, cell in self.cells.items():

value = data.get(key, "")

cell.setText(str(value))