1. 不要迷恋停止单,它缺点多的很

当你想以比市场价更高的价格买,或者以比市场价更低的价格卖时,使用send_order()是会立即执行的,但是用停止单却可以做到这一点,这是停止单的优点。

但是实际使用中停止单也是有缺点的:

- 当以比市场价更低的价格买,它会立即被执行

- 当以比市场价更高的价格卖,它会立即被执行

- 实际运行中有多个停止单通知满足条件,接口在极短时间内接受多个停止单发出的委托,发生委托覆盖。表现为明明策略发出过多个停止单,但是只有最后一个停止单有结果,其他的委托莫名其妙的人间蒸发了,不见了,接口不回应、不通知,策略也不知道,用户无法查。

- 停止单一经发出,触发价也是执行价,无法根据当时的市场价格做出价格调整

- 只有CTA策略才可以使用停止单,其他类型的策略无法使用,因为它的执行逻辑和具体合约耦合度太高

2. 什么是条件单?

这是本人给它取的名字,它其实是本人以前提到的交易线(TradeLine)的改进和增强。

它主要就是为解决停止单上述缺点而设计的,当然应该具备上述优点。

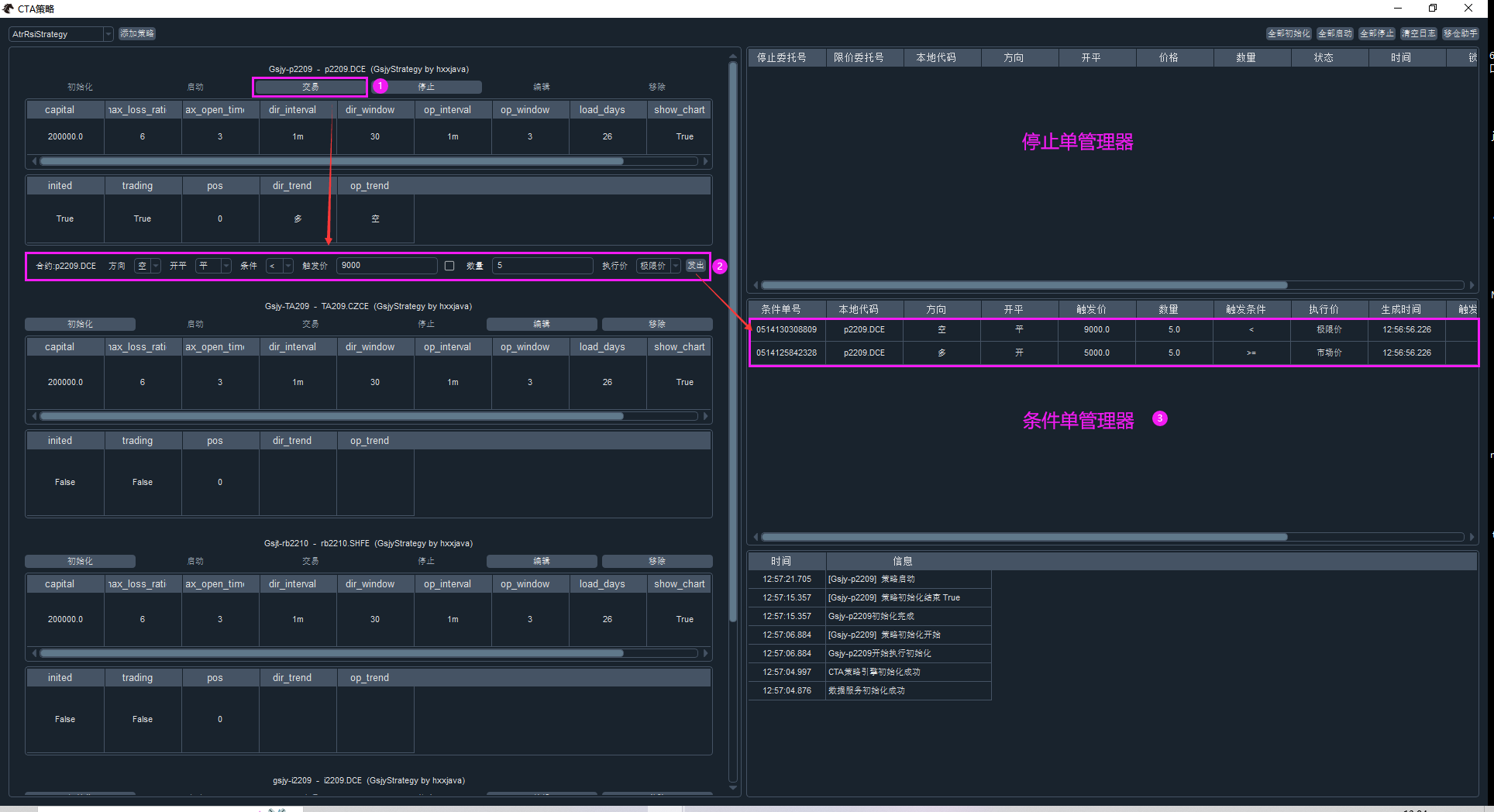

- 可以设定触发价格和触发条件

- 触发条件包括四种:>=、<=、>、<,与执行的委托方向无关

- 当市场价格满足触发条件时,条件单立即执行,执行收最小流控限制

- 执行价格可以是触发价、市场价或极限价(买时为涨停价,卖时为跌停价)

- 条件单管理器还可以提供手工取消条件单的功能,双击就可以取消

先看一眼条件单的效果图

2.1 它数据结构包含如下:

在vnpy_ctastrategy\base.py中增加如下代码:

class Condition(Enum): # hxxjava add

""" 条件单的条件 """

BT = ">"

LT = "<"

BE = ">="

LE = "<="

class ExecutePrice(Enum): # hxxjava add

""" 执行价格 """

SETPRICE = "设定价"

MARKET = "市场价"

EXTREME = "极限价"

class CondOrderStatus(Enum): # hxxjava add

""" 条件单状态 """

WAITING = "等待中"

CANCELLED = "已撤销"

TRIGGERED = "已触发"

@dataclass

class ConditionOrder: # hxxjava add

""" 条件单 """

strategy_name: str

vt_symbol: str

direction: Direction

offset: Offset

price: float

volume: float

condition:Condition

execute_price:ExecutePrice = ExecutePrice.SETPRICE

create_time: datetime = datetime.now()

trigger_time: datetime = None

cond_orderid: str = "" # 条件单编号

status: CondOrderStatus = CondOrderStatus.WAITING

def __post_init__(self):

""" """

if not self.cond_orderid:

self.cond_orderid = datetime.now().strftime("%m%d%H%M%S%f")[:13]

EVENT_CONDITION_ORDER = "eConditionOrder" # hxxjava add2.2 条件单管理器

2.2.1 修改CTA策略管理器

修改vnpy_ctastrategy\ui\widget.py中的class CtaManager,代码如下:

class CtaManager(QtWidgets.QWidget):

""""""

signal_log: QtCore.Signal = QtCore.Signal(Event)

signal_strategy: QtCore.Signal = QtCore.Signal(Event)

def __init__(self, main_engine: MainEngine, event_engine: EventEngine) -> None:

""""""

super().__init__()

self.main_engine: MainEngine = main_engine

self.event_engine: EventEngine = event_engine

self.cta_engine: CtaEngine = main_engine.get_engine(APP_NAME)

self.managers: Dict[str, StrategyManager] = {}

self.init_ui()

self.register_event()

self.cta_engine.init_engine()

self.update_class_combo()

def init_ui(self) -> None:

""""""

self.setWindowTitle("CTA策略")

# Create widgets

self.class_combo: QtWidgets.QComboBox = QtWidgets.QComboBox()

add_button: QtWidgets.QPushButton = QtWidgets.QPushButton("添加策略")

add_button.clicked.connect(self.add_strategy)

init_button: QtWidgets.QPushButton = QtWidgets.QPushButton("全部初始化")

init_button.clicked.connect(self.cta_engine.init_all_strategies)

start_button: QtWidgets.QPushButton = QtWidgets.QPushButton("全部启动")

start_button.clicked.connect(self.cta_engine.start_all_strategies)

stop_button: QtWidgets.QPushButton = QtWidgets.QPushButton("全部停止")

stop_button.clicked.connect(self.cta_engine.stop_all_strategies)

clear_button: QtWidgets.QPushButton = QtWidgets.QPushButton("清空日志")

clear_button.clicked.connect(self.clear_log)

roll_button: QtWidgets.QPushButton = QtWidgets.QPushButton("移仓助手")

roll_button.clicked.connect(self.roll)

self.scroll_layout: QtWidgets.QVBoxLayout = QtWidgets.QVBoxLayout()

self.scroll_layout.addStretch()

scroll_widget: QtWidgets.QWidget = QtWidgets.QWidget()

scroll_widget.setLayout(self.scroll_layout)

self.scroll_area: QtWidgets.QScrollArea = QtWidgets.QScrollArea()

self.scroll_area.setWidgetResizable(True)

self.scroll_area.setWidget(scroll_widget)

self.log_monitor: LogMonitor = LogMonitor(self.main_engine, self.event_engine)

self.stop_order_monitor: StopOrderMonitor = StopOrderMonitor(

self.main_engine, self.event_engine

)

self.strategy_combo = QtWidgets.QComboBox()

self.strategy_combo.setMinimumWidth(200)

find_button = QtWidgets.QPushButton("查找")

find_button.clicked.connect(self.find_strategy)

# hxxjava add

self.condition_order_monitor = ConditionOrderMonitor(self.cta_engine)

# Set layout

hbox1: QtWidgets.QHBoxLayout = QtWidgets.QHBoxLayout()

hbox1.addWidget(self.class_combo)

hbox1.addWidget(add_button)

hbox1.addStretch()

hbox1.addWidget(self.strategy_combo)

hbox1.addWidget(find_button)

hbox1.addStretch()

hbox1.addWidget(init_button)

hbox1.addWidget(start_button)

hbox1.addWidget(stop_button)

hbox1.addWidget(clear_button)

hbox1.addWidget(roll_button)

grid = QtWidgets.QGridLayout()

# grid.addWidget(self.scroll_area, 0, 0, 2, 1)

grid.addWidget(self.scroll_area, 0, 0, 3, 1) # hxxjava change 3 rows , 1 column

grid.addWidget(self.stop_order_monitor, 0, 1)

grid.addWidget(self.condition_order_monitor, 1, 1) # hxxjava add

# grid.addWidget(self.log_monitor, 1, 1)

grid.addWidget(self.log_monitor, 2, 1) # hxxjava change

vbox: QtWidgets.QVBoxLayout = QtWidgets.QVBoxLayout()

vbox.addLayout(hbox1)

vbox.addLayout(grid)

self.setLayout(vbox)

def update_class_combo(self) -> None:

""""""

names = self.cta_engine.get_all_strategy_class_names()

names.sort()

self.class_combo.addItems(names)

def update_strategy_combo(self) -> None:

""""""

names = list(self.managers.keys())

names.sort()

self.strategy_combo.clear()

self.strategy_combo.addItems(names)

def register_event(self) -> None:

""""""

self.signal_strategy.connect(self.process_strategy_event)

self.event_engine.register(

EVENT_CTA_STRATEGY, self.signal_strategy.emit

)

def process_strategy_event(self, event) -> None:

"""

Update strategy status onto its monitor.

"""

data = event.data

strategy_name: str = data["strategy_name"]

if strategy_name in self.managers:

manager: StrategyManager = self.managers[strategy_name]

manager.update_data(data)

else:

manager: StrategyManager = StrategyManager(self, self.cta_engine, data)

self.scroll_layout.insertWidget(0, manager)

self.managers[strategy_name] = manager

self.update_strategy_combo()

def remove_strategy(self, strategy_name) -> None:

""""""

manager: StrategyManager = self.managers.pop(strategy_name)

manager.deleteLater()

self.update_strategy_combo()

def add_strategy(self) -> None:

""""""

class_name: str = str(self.class_combo.currentText())

if not class_name:

return

parameters: dict = self.cta_engine.get_strategy_class_parameters(class_name)

editor: SettingEditor = SettingEditor(parameters, class_name=class_name)

n: int = editor.exec_()

if n == editor.Accepted:

setting: dict = editor.get_setting()

vt_symbol: str = setting.pop("vt_symbol")

strategy_name: str = setting.pop("strategy_name")

self.cta_engine.add_strategy(

class_name, strategy_name, vt_symbol, setting

)

def find_strategy(self) -> None:

""""""

strategy_name = self.strategy_combo.currentText()

manager = self.managers[strategy_name]

self.scroll_area.ensureWidgetVisible(manager)

def clear_log(self) -> None:

""""""

self.log_monitor.setRowCount(0)

def show(self) -> None:

""""""

self.showMaximized()

def roll(self) -> None:

""""""

dialog: RolloverTool = RolloverTool(self)

dialog.exec_()2.2.2 条件单管理器代码

在vnpy_ctastrategy\ui\widget.py中增加如下代码:

class ConditionOrderMonitor(BaseMonitor): # hxxjava add

"""

Monitor for condition order.

"""

event_type = EVENT_CONDITION_ORDER

data_key = "cond_orderid"

sorting = True

headers = {

"cond_orderid": {

"display": "条件单号",

"cell": BaseCell,

"update": False,

},

"vt_symbol": {"display": "本地代码", "cell": BaseCell, "update": False},

"direction": {"display": "方向", "cell": EnumCell, "update": False},

"offset": {"display": "开平", "cell": EnumCell, "update": False},

"price": {"display": "触发价", "cell": BaseCell, "update": False},

"volume": {"display": "数量", "cell": BaseCell, "update": False},

"condition": {"display": "触发条件", "cell": EnumCell, "update": False},

"execute_price": {"display": "执行价", "cell": EnumCell, "update": False},

"create_time": {"display": "生成时间", "cell": TimeCell, "update": False},

"trigger_time": {"display": "触发时间", "cell": TimeCell, "update": False},

"status": {"display": "状态", "cell": EnumCell, "update": True},

"strategy_name": {"display": "策略名称", "cell": BaseCell, "update": False},

}

def __init__(self,cta_engine : MyCtaEngine):

""""""

super().__init__(cta_engine.main_engine, cta_engine.event_engine)

self.cta_engine = cta_engine

def init_ui(self):

"""

Connect signal.

"""

super().init_ui()

self.setToolTip("双击单元格可停止条件单")

self.itemDoubleClicked.connect(self.stop_condition_order)

def stop_condition_order(self, cell):

"""

Stop algo if cell double clicked.

"""

order = cell.get_data()

if order:

self.cta_engine.cancel_condition_order(order.cond_orderid)2.2.3 加载条件单管理器

修改策略管理器StrategyManager的代码如下:

class StrategyManager(QtWidgets.QFrame):

"""

Manager for a strategy

"""

def __init__(

self, cta_manager: CtaManager, cta_engine: CtaEngine, data: dict

):

""""""

super(StrategyManager, self).__init__()

self.cta_manager = cta_manager

self.cta_engine = cta_engine

self.strategy_name = data["strategy_name"]

self._data = data

self.tradetool : TradingWidget = None # hxxjava add

self.init_ui()

def init_ui(self):

""""""

self.setFixedHeight(300)

self.setFrameShape(self.Box)

self.setLineWidth(1)

self.init_button = QtWidgets.QPushButton("初始化")

self.init_button.clicked.connect(self.init_strategy)

self.start_button = QtWidgets.QPushButton("启动")

self.start_button.clicked.connect(self.start_strategy)

self.start_button.setEnabled(False)

self.stop_button = QtWidgets.QPushButton("停止")

self.stop_button.clicked.connect(self.stop_strategy)

self.stop_button.setEnabled(False)

self.trade_button = QtWidgets.QPushButton("交易") # hxxjava add

self.trade_button.clicked.connect(self.show_tradetool) # hxxjava add

self.trade_button.setEnabled(False) # hxxjava add

self.edit_button = QtWidgets.QPushButton("编辑")

self.edit_button.clicked.connect(self.edit_strategy)

self.remove_button = QtWidgets.QPushButton("移除")

self.remove_button.clicked.connect(self.remove_strategy)

strategy_name = self._data["strategy_name"]

vt_symbol = self._data["vt_symbol"]

class_name = self._data["class_name"]

author = self._data["author"]

label_text = (

f"{strategy_name} - {vt_symbol} ({class_name} by {author})"

)

label = QtWidgets.QLabel(label_text)

label.setAlignment(QtCore.Qt.AlignCenter)

self.parameters_monitor = DataMonitor(self._data["parameters"])

self.variables_monitor = DataMonitor(self._data["variables"])

hbox = QtWidgets.QHBoxLayout()

hbox.addWidget(self.init_button)

hbox.addWidget(self.start_button)

hbox.addWidget(self.trade_button) # hxxjava add

hbox.addWidget(self.stop_button)

hbox.addWidget(self.edit_button)

hbox.addWidget(self.remove_button)

# hxxjava change to self.vbox,old is vbox

self.vbox = QtWidgets.QVBoxLayout()

self.vbox.addWidget(label)

self.vbox.addLayout(hbox)

self.vbox.addWidget(self.parameters_monitor)

self.vbox.addWidget(self.variables_monitor)

self.setLayout(self.vbox)

def update_data(self, data: dict):

""""""

self._data = data

self.parameters_monitor.update_data(data["parameters"])

self.variables_monitor.update_data(data["variables"])

# Update button status

variables = data["variables"]

inited = variables["inited"]

trading = variables["trading"]

if not inited:

return

self.init_button.setEnabled(False)

if trading:

self.start_button.setEnabled(False)

self.trade_button.setEnabled(True) # hxxjava

self.stop_button.setEnabled(True)

self.edit_button.setEnabled(False)

self.remove_button.setEnabled(False)

else:

self.start_button.setEnabled(True)

self.trade_button.setEnabled(False) # hxxjava

self.stop_button.setEnabled(False)

self.edit_button.setEnabled(True)

self.remove_button.setEnabled(True)

def init_strategy(self):

""""""

self.cta_engine.init_strategy(self.strategy_name)

def start_strategy(self):

""""""

self.cta_engine.start_strategy(self.strategy_name)

def show_tradetool(self): # hxxjava add

""" 为策略显示交易工具 """

if not self.tradetool:

strategy = self.cta_engine.strategies.get(self.strategy_name,None)

if strategy and strategy.trading:

self.tradetool = TradingWidget(strategy,self.cta_engine.event_engine)

self.vbox.addWidget(self.tradetool)

else:

is_visible = self.tradetool.isVisible()

self.tradetool.setVisible(not is_visible)

def stop_strategy(self):

""""""

self.cta_engine.stop_strategy(self.strategy_name)

def edit_strategy(self):

""""""

strategy_name = self._data["strategy_name"]

parameters = self.cta_engine.get_strategy_parameters(strategy_name)

editor = SettingEditor(parameters, strategy_name=strategy_name)

n = editor.exec_()

if n == editor.Accepted:

setting = editor.get_setting()

self.cta_engine.edit_strategy(strategy_name, setting)

def remove_strategy(self):

""""""

result = self.cta_engine.remove_strategy(self.strategy_name)

# Only remove strategy gui manager if it has been removed from engine

if result:

self.cta_manager.remove_strategy(self.strategy_name)2.2.4 交易组件

创建vnpy\usertools\trading_widget.py文件,其中内容:

"""

条件单交易组件

作者:hxxjava

日线:2022-5-10

"""

from vnpy.trader.ui import QtCore, QtWidgets, QtGui

from vnpy.trader.constant import Direction,Offset

from vnpy.trader.event import EVENT_TICK

from vnpy.event.engine import Event,EventEngine

from vnpy_ctastrategy.base import Condition,CondOrderStatus,ExecutePrice,ConditionOrder

from vnpy_ctastrategy.template import CtaTemplate

class TradingWidget(QtWidgets.QWidget):

"""

CTA strategy manual trading widget.

"""

signal_tick = QtCore.pyqtSignal(Event)

def __init__(self, strategy: CtaTemplate, event_engine: EventEngine):

""""""

super().__init__()

self.strategy: CtaTemplate = strategy

self.event_engine: EventEngine = event_engine

self.vt_symbol: str = strategy.vt_symbol

self.price_digits: int = 0

self.init_ui()

self.register_event()

def init_ui(self) -> None:

""""""

# 交易方向:多/空

self.direction_combo = QtWidgets.QComboBox()

self.direction_combo.addItems(

[Direction.LONG.value, Direction.SHORT.value])

# 开平选择:开/平

self.offset_combo = QtWidgets.QComboBox()

self.offset_combo.addItems([offset.value for offset in Offset])

# 条件类型

conditions = [Condition.BE,Condition.LE,Condition.BT,Condition.LT]

self.condition_combo = QtWidgets.QComboBox()

self.condition_combo.addItems(

[condition.value for condition in conditions])

double_validator = QtGui.QDoubleValidator()

double_validator.setBottom(0)

self.price_line = QtWidgets.QLineEdit()

self.price_line.setValidator(double_validator)

self.exit_line = QtWidgets.QLineEdit()

self.exit_line.setValidator(double_validator)

self.volume_line = QtWidgets.QLineEdit()

self.volume_line.setValidator(double_validator)

self.price_check = QtWidgets.QCheckBox()

self.price_check.setToolTip("设置价格随行情更新")

execute_prices = [ExecutePrice.SETPRICE,ExecutePrice.MARKET,ExecutePrice.EXTREME]

self.execute_price_combo = QtWidgets.QComboBox()

self.execute_price_combo.addItems(

[execute_price.value for execute_price in execute_prices])

send_button = QtWidgets.QPushButton("发出")

send_button.clicked.connect(self.send_condition_order)

hbox = QtWidgets.QHBoxLayout()

hbox.addWidget(QtWidgets.QLabel(f"合约:{self.vt_symbol}"))

hbox.addWidget(QtWidgets.QLabel("方向"))

hbox.addWidget(self.direction_combo)

hbox.addWidget(QtWidgets.QLabel("开平"))

hbox.addWidget(self.offset_combo)

hbox.addWidget(QtWidgets.QLabel("条件"))

hbox.addWidget(self.condition_combo)

hbox.addWidget(QtWidgets.QLabel("触发价"))

hbox.addWidget(self.price_line)

hbox.addWidget(self.price_check)

hbox.addWidget(QtWidgets.QLabel("数量"))

hbox.addWidget(self.volume_line)

hbox.addWidget(QtWidgets.QLabel("执行价"))

hbox.addWidget(self.execute_price_combo)

hbox.addWidget(send_button)

# Overall layout

self.setLayout(hbox)

def register_event(self) -> None:

""""""

self.signal_tick.connect(self.process_tick_event)

self.event_engine.register(EVENT_TICK, self.signal_tick.emit)

def process_tick_event(self, event: Event) -> None:

""""""

tick = event.data

if tick.vt_symbol != self.vt_symbol:

return

if self.price_check.isChecked():

self.price_line.setText(f"{tick.last_price}")

def send_condition_order(self) -> bool:

"""

Send new order manually.

"""

try:

direction = Direction(self.direction_combo.currentText())

offset = Offset(self.offset_combo.currentText())

condition = Condition(self.condition_combo.currentText())

price = float(self.price_line.text())

volume = float(self.volume_line.text())

execute_price = ExecutePrice(self.execute_price_combo.currentText())

order = ConditionOrder(

strategy_name = self.strategy.strategy_name,

vt_symbol=self.vt_symbol,

direction=direction,

offset=offset,

price=price,

volume=volume,

condition=condition,

execute_price=execute_price

)

self.strategy.send_condition_order(order=order)

print(f"发出条件单 : vt_symbol={self.vt_symbol},success ! {order}")

return True

except:

print(f"发出条件单 : vt_symbol={self.vt_symbol},input error !")

return False2.3 有条件单功能的CTA引擎——MyCtaEngine

2.3.1 MyCtaEngine的实现

在vnpy_ctastrategy\engine.py中对CtaEngine进行如下扩展:

class MyCtaEngine(CtaEngine):

""" """

condition_filename = "condition_order.json" # 历史条件单存储文件

def __init__(self, main_engine: MainEngine, event_engine: EventEngine):

""""""

super().__init__(main_engine,event_engine)

self.condition_orders:Dict[str,ConditionOrder] = {} # strategy_name: dict

def load_active_condtion_orders(self):

""" """

return {}

def process_tick_event(self,event:Event):

""" 用tick的价格检查条件单 """

super().process_tick_event(event)

tick:TickData = event.data

all_condition_orders = [order for order in self.condition_orders.values() \

if order.vt_symbol == tick.vt_symbol and order.status == CondOrderStatus.WAITING]

for order in all_condition_orders:

# 检查条件单是否满足条件

self.check_condition_order(order,tick)

def check_condition_order(self,order:ConditionOrder,tick:TickData):

""" 检查条件单是否满足条件 """

strategy = self.strategies.get(order.strategy_name,None)

if not strategy or not strategy.trading:

return False

price = tick.last_price

is_be = order.condition == Condition.BE and price >= order.price

is_le = order.condition == Condition.LE and price <= order.price

is_bt = order.condition == Condition.BT and price > order.price

is_lt = order.condition == Condition.LT and price < order.price

if is_be or is_le or is_bt or is_lt:

# 满足触发条件

if order.execute_price == ExecutePrice.MARKET:

# 取市场价

price = tick.last_price

elif order.execute_price == ExecutePrice.EXTREME:

# 取极限价

price = tick.limit_up if order.direction == Direction.LONG else tick.limit_down

else:

# 取设定价

price = order.price

# 执行委托

order_ids = strategy.send_order(

direction = order.direction,

offset=order.offset,

price=price,

volume=order.volume

)

if order_ids:

order.trigger_time = tick.datetime

order.status = CondOrderStatus.TRIGGERED

self.event_engine.put(Event(EVENT_CONDITION_ORDER,order))

def send_condition_order(self,order:ConditionOrder):

""" """

strategy = self.strategies.get(order.strategy_name,None)

if not strategy or not strategy.trading:

return False

if order.cond_orderid not in self.condition_orders:

self.condition_orders[order.cond_orderid] = order

self.event_engine.put(Event(EVENT_CONDITION_ORDER,order))

return True

return False

def cancel_condition_order(self,cond_orderid:str):

""" """

order:ConditionOrder = self.condition_orders.get(cond_orderid,None)

if not order:

return False

order.status = CondOrderStatus.CANCELLED

self.event_engine.put(Event(EVENT_CONDITION_ORDER,order))

return True

def cancel_all_condition_orders(self,strategy_name:str):

""" """

for order in self.condition_orders.values():

if order.strategy_name == strategy_name and order.status == CondOrderStatus.WAITING:

order.status = CondOrderStatus.CANCELLED

self.call_strategy_func(strategy,strategy.on_condition_order)

self.event_engine.put(Event(EVENT_CONDITION_ORDER,order))

return True2.3.2 更换CtaEngine

对vnpy_ctastrategy__init__.py中的CtaTemplate进行如下修改:

from .engine import MyCtaEngine # hxxjava addclass CtaStrategyApp(BaseApp):

""""""

app_name = APP_NAME

app_module = __module__

app_path = Path(__file__).parent

display_name = "CTA策略"

# engine_class = CtaEngine

engine_class = MyCtaEngine # hxxjava add

widget_name = "CtaManager"

icon_name = str(app_path.joinpath("ui", "cta.ico"))2.3.3 对CtaTemplate进行扩展

对vnpy_ctastrategy\template.py中的CtaTemplate进行如下扩展:

@virtual

def on_condition_order(self, cond_order: ConditionOrder):

"""

Callback of condition order update.

"""

pass

def send_condition_order(self,order:ConditionOrder): # hxxjava add

""" """

if not self.trading:

return False

return self.cta_engine.send_condition_order(order)

def cancel_condition_order(self,cond_orderid:str): # hxxjava add

""" """

return self.cta_engine.cancel_condition_order(cond_orderid)

def cancel_all_condition_orders(self): # hxxjava add

""" """

return self.cta_engine.cancel_all_condition_orders(self)2.3.4 CTA用户策略中如何使用条件单功能

1)CTA策略中的条件单被触发点回调通知:

def on_condition_order(self, cond_order: ConditionOrder):

"""

Callback of condition order update.

"""

print(f"条件单已经执行,cond_order = {cond_order}")2)发起条件单

cond_order = ConditionOrder(... ...)

self.send_condition_order(cond_order)3)取消条件单

self.cancel_condition_order(cond_orderid)4)取消策略的所有条件单

self.cancel_all_condition_orders()3. 条件单应该在vnpy系统中被广泛使用

- 它应该运行在整个vnpy系统的底层,为各类的应用策略提供委托支持,

- 对连续密集触发点条件单实施流控限制,避免交易接口出现丢单的流控问题

- 各类应用的引擎应该提供send_condition_order()接口,实现条件单到不同应用委托执行逻辑

- 各类应用的模板应该提供on_condition_order回调,解决条件单触发后对不同类型用户策略的触发通知

- 用户策略尽量使用条件单来执行交易,避免直接执行来自接口的委托函数