期货部分合约有10:15-10:30停盘休息时间,如果按照vnpy原有K线合成逻辑操作,合成出来的周期K线多数情况下都是错误的,在使用前需要对合成逻辑进行修改。

以下合成逻辑修改仅适合从数据库读取1分钟K线数据再合成情况,其它数据来源自己斟酌是否适用。不保证以下修改逻辑完全正确,只做抛砖引玉之用,望大家共享参与探讨。

(注:以下代码注释部分为修改部分)

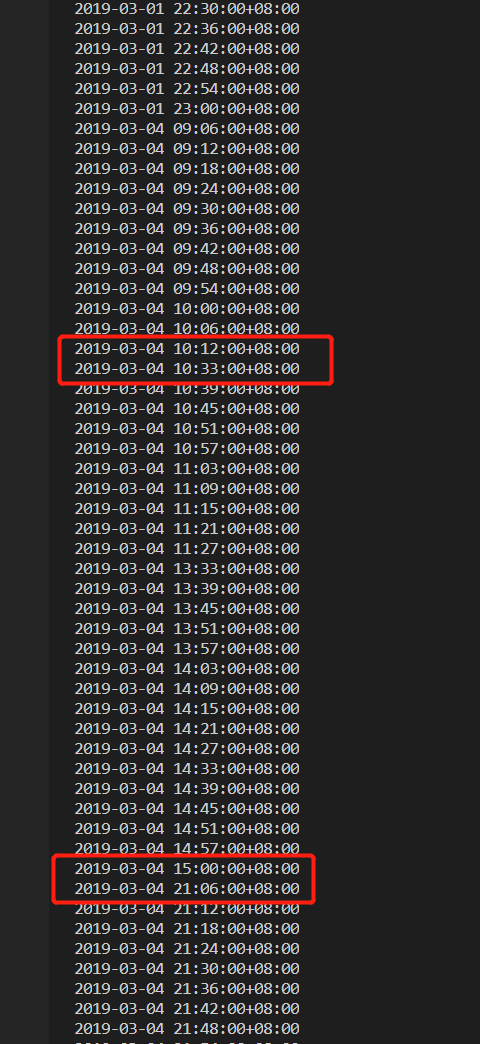

合成后的数据时间截图如下

class BarGenerator:

"""

For:

1. generating 1 minute bar data from tick data

2. generateing x minute bar/x hour bar data from 1 minute data

Notice:

1. for x minute bar, x must be able to divide 60: 2, 3, 5, 6, 10, 15, 20, 30

2. for x hour bar, x can be any number

"""

def __init__(

self,

on_bar: Callable,

window: int = 0,

on_window_bar: Callable = None,

interval: Interval = Interval.MINUTE

):

"""Constructor"""

self.bar: BarData = None

self.on_bar: Callable = on_bar

self.interval: Interval = interval

self.interval_count: int = 0

self.interval_minute: int = 0 # 此处增加一个变量,用于记数K线条数。

self.hour_bar: BarData = None

self.window: int = window

self.window_bar: BarData = None

self.on_window_bar: Callable = on_window_bar

self.last_tick: TickData = None

self.last_bar: BarData = None

def update_tick(self, tick: TickData) -> None:

"""

Update new tick data into generator.

"""

new_minute = False

# Filter tick data with 0 last price

if not tick.last_price:

return

# Filter tick data with older timestamp

if self.last_tick and tick.datetime < self.last_tick.datetime:

return

if not self.bar:

new_minute = True

elif (

(self.bar.datetime.minute != tick.datetime.minute)

or (self.bar.datetime.hour != tick.datetime.hour)

):

self.bar.datetime = self.bar.datetime.replace(

second=0, microsecond=0

)

self.on_bar(self.bar)

new_minute = True

if new_minute:

self.bar = BarData(

symbol=tick.symbol,

exchange=tick.exchange,

interval=Interval.MINUTE,

datetime=tick.datetime,

gateway_name=tick.gateway_name,

open_price=tick.last_price,

high_price=tick.last_price,

low_price=tick.last_price,

close_price=tick.last_price,

open_interest=tick.open_interest

)

else:

self.bar.high_price = max(self.bar.high_price, tick.last_price)

if tick.high_price > self.last_tick.high_price:

self.bar.high_price = max(self.bar.high_price, tick.high_price)

self.bar.low_price = min(self.bar.low_price, tick.last_price)

if tick.low_price < self.last_tick.low_price:

self.bar.low_price = min(self.bar.low_price, tick.low_price)

self.bar.close_price = tick.last_price

self.bar.open_interest = tick.open_interest

self.bar.datetime = tick.datetime

if self.last_tick:

volume_change = tick.volume - self.last_tick.volume

self.bar.volume += max(volume_change, 0)

self.last_tick = tick

def update_bar(self, bar: BarData) -> None:

"""

Update 1 minute bar into generator

"""

if self.interval == Interval.MINUTE:

self.update_bar_minute_window(bar)

else:

self.update_bar_hour_window(bar)

def update_bar_minute_window(self, bar: BarData) -> None:

""""""

# If not inited, create window bar object

if not self.window_bar:

dt = bar.datetime.replace(second=0, microsecond=0)

self.window_bar = BarData(

symbol=bar.symbol,

exchange=bar.exchange,

datetime=dt,

gateway_name=bar.gateway_name,

open_price=bar.open_price,

high_price=bar.high_price,

low_price=bar.low_price

)

# Otherwise, update high/low price into window bar

else:

-------以下为K线合成逻辑主要修改部分:

self.window_bar.datetime = bar.datetime

self.window_bar.high_price = max(

self.window_bar.high_price,

bar.high_price

)

self.window_bar.low_price = min(

self.window_bar.low_price,

bar.low_price

)

# Update close price/volume into window bar

self.window_bar.close_price = bar.close_price

self.window_bar.volume += int(bar.volume)

self.window_bar.open_interest = bar.open_interest

-------以下为K线合成逻辑主要修改部分

# Check if window bar completed

self.interval_minute += 1

if not self.interval_minute % self.window:

self.interval_minute = 0

self.on_window_bar(self.window_bar)

self.window_bar = None

elif bar.datetime.time() == time(15, 00):

self.interval_minute = 0

self.on_window_bar(self.window_bar)

self.window_bar = None

------修改结束————

- list text here

以下代码略# Cache last bar object self.last_bar = bar

以下为6分钟周期K线合成后的时间截图