之前试过aksahre或者自己写爬虫爬取数据,数据获取耗时久且不稳定,主要是脚本维护不容易,这里推荐一个相对容易且免费的方式

先打开ricequant的投资研究板块,进入jupyter notebook,开启一个新的,先获取期货市场所有的上市合约字段头,然后使用get_price获取想要时段的数据

示例 2010-2024-5-31的日频数据,保存,然后退出点击下载即可获得数据

get_info = all_instruments(type='Future')

test_df = get_price(get_info['order_book_id'], start_date='2010-01-01', end_date='2024-05-31', frequency='1d', fields=None, adjust_type='pre', skip_suspended =False, market='cn', expect_df=True,time_slice=None)

test_df.to_csv('daily_bar.csv')

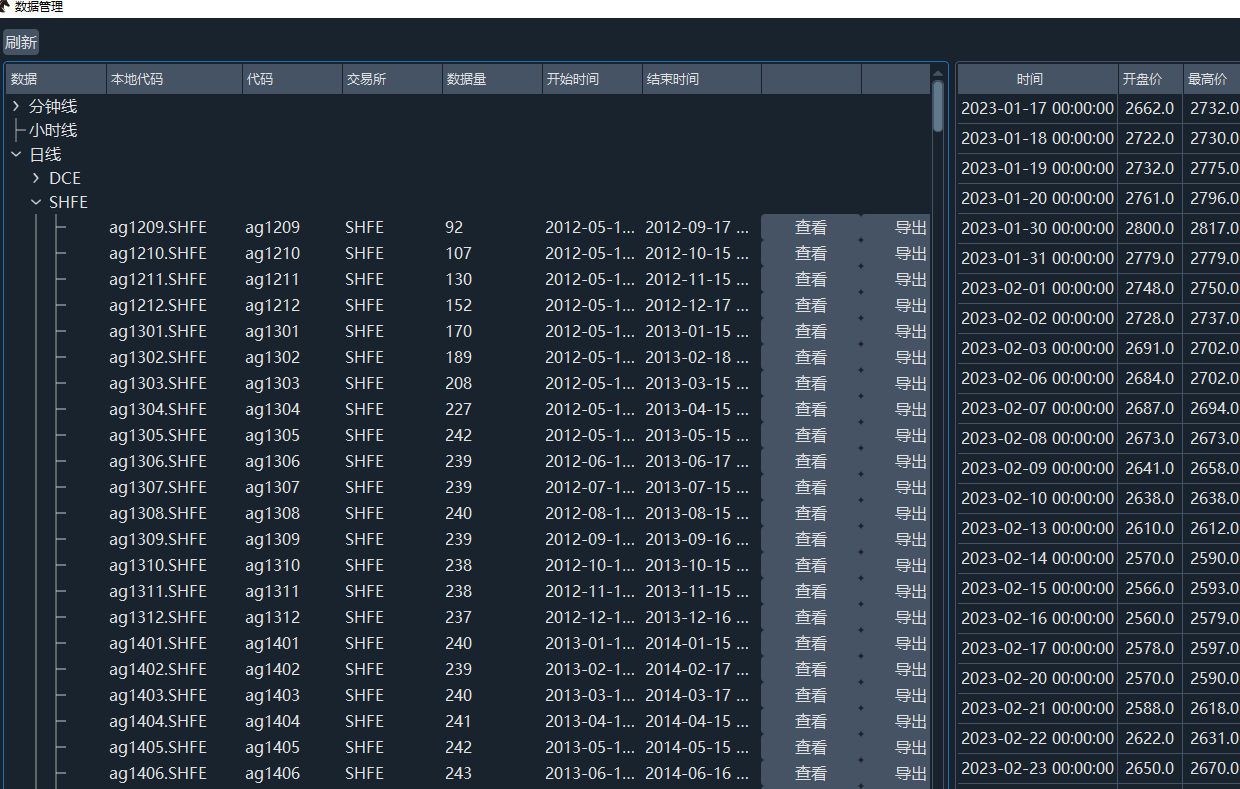

之后再在本地开个jupyter,使用pandas打开daily_bar.csv

from vnpy.trader.constant import (Exchange, Interval)

import pandas as pd

from vnpy.trader.database import get_database

from vnpy.trader.object import (BarData,TickData)

from datetime import datetime

from pytz import timezone

import json

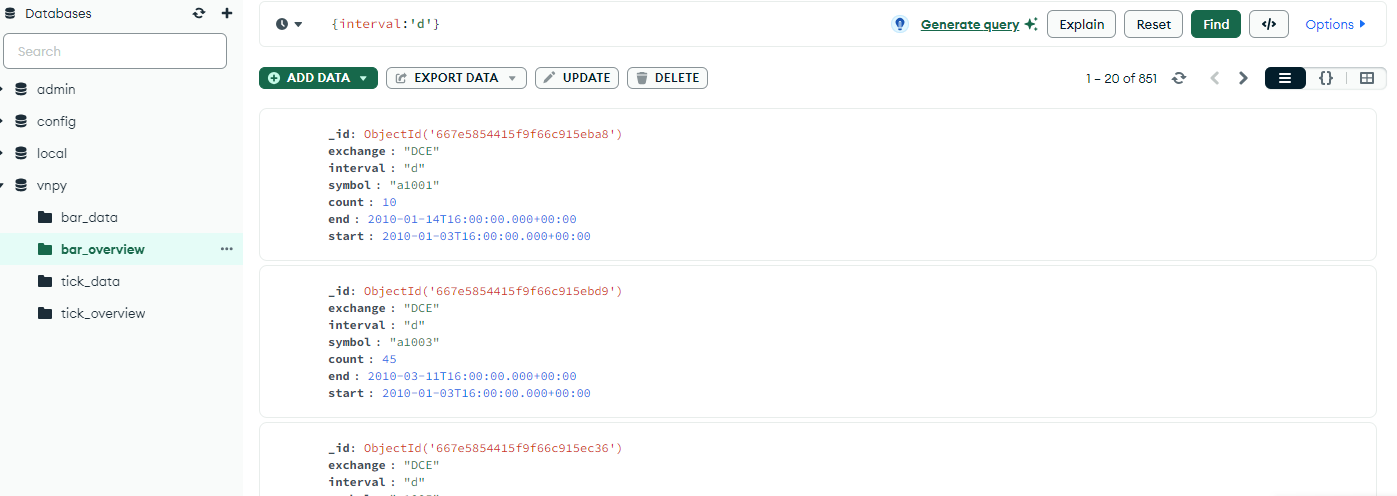

database_manager = get_database()

tz = timezone( "Asia/Shanghai")

f = open('code_info.json','r')

content = f.read()

json_file = json.loads(content)

f.close()

def move_df_to_mongodb(imported_data:pd.DataFrame,collection_name:str,interval='d'):

bars = []

start = None

count = 0

interval = Interval(interval)

if '88' in collection_name:

exchange_code = (collection_name.split('88')[0]).upper()

elif '99' in collection_name:

exchange_code = (collection_name.split('99')[0]).upper()

else:

exchange_code = (collection_name[:-4]).upper()

try:

code_exchange = Exchange(json_file[exchange_code]['exchange'])

except:

print(f'合约{exchange_code} 无法查询到交易所代码,请查看json文件或合约信息')

return

for row in imported_data.itertuples():

# print(interval)

bar = BarData(

symbol=row.symbol,

exchange=code_exchange,

datetime=tz.localize(datetime.fromisoformat(row.datetime)),

#datetime=row.datetime.replace(tzinfo=utc_8),

interval=interval,

volume=row.volume,

open_price=row.open,

high_price=row.high,

low_price=row.low,

close_price=row.close,

open_interest=row.open_interest,

turnover=row.total_turnover,

gateway_name = 'DB'

)

bars.append(bar)

# do some statistics

count += 1

if not start:

start = bar.datetime

end = bar.datetime

# insert into database

database_manager.save_bar_data(bars)

print(f"Insert Bar {collection_name}: {count} from {start} - {end}")

def load_ricequant_df(rice_df):

daily_grups = rice_df.groupby('order_book_id')

code_ls = daily_grups.groups.keys()

for codex in code_ls:

load_df = daily_grups.get_group(codex).copy()

load_df = load_df[['order_book_id','date','open','high','low','close','volume','total_turnover','open_interest']]

load_df.columns = ['symbol','datetime','open','high','low','close','volume','total_turnover','open_interest']

load_df.symbol = load_df.symbol.str.lower()

print(f'开始导入 {codex} 行情')

move_df_to_mongodb(load_df,collection_name=codex)

daily_df = pd.read_csv('daily_bar.csv')

load_ricequant_df(daily_df)

文件链接:

链接:https://pan.baidu.com/s/1dylBHApYsyLDoIjeLM_UVA?pwd=rxa7

提取码:rxa7

PS:

理论上也能从ricequant中获取分钟k然后再导入进vnpy数据库,代码构造类似。我没有尝试过(据估算分钟数据大约有30g,这可能需要按品种一个一个搬)。后面有时间探讨分钟k数据和更新方式。

PPS:

数据导入方式参考:

https://www.vnpy.com/forum/topic/3759-vn-pyshe-qu-jing-xuan-22-kan-wan-zhe-pian-che-di-xue-hui-csvli-shi-shu-ju-dao-ru?page=1

https://www.vnpy.com/forum/topic/3203-bian-xie-pythonjiao-ben-shi-xian-shu-ju-ru-ku